Risk-Sensitive Policy Optimization via Predictive CVaR Policy Gradient

Ju-Hyun Kim ⋅ Seungki Min

2024 Poster

{kind=link}

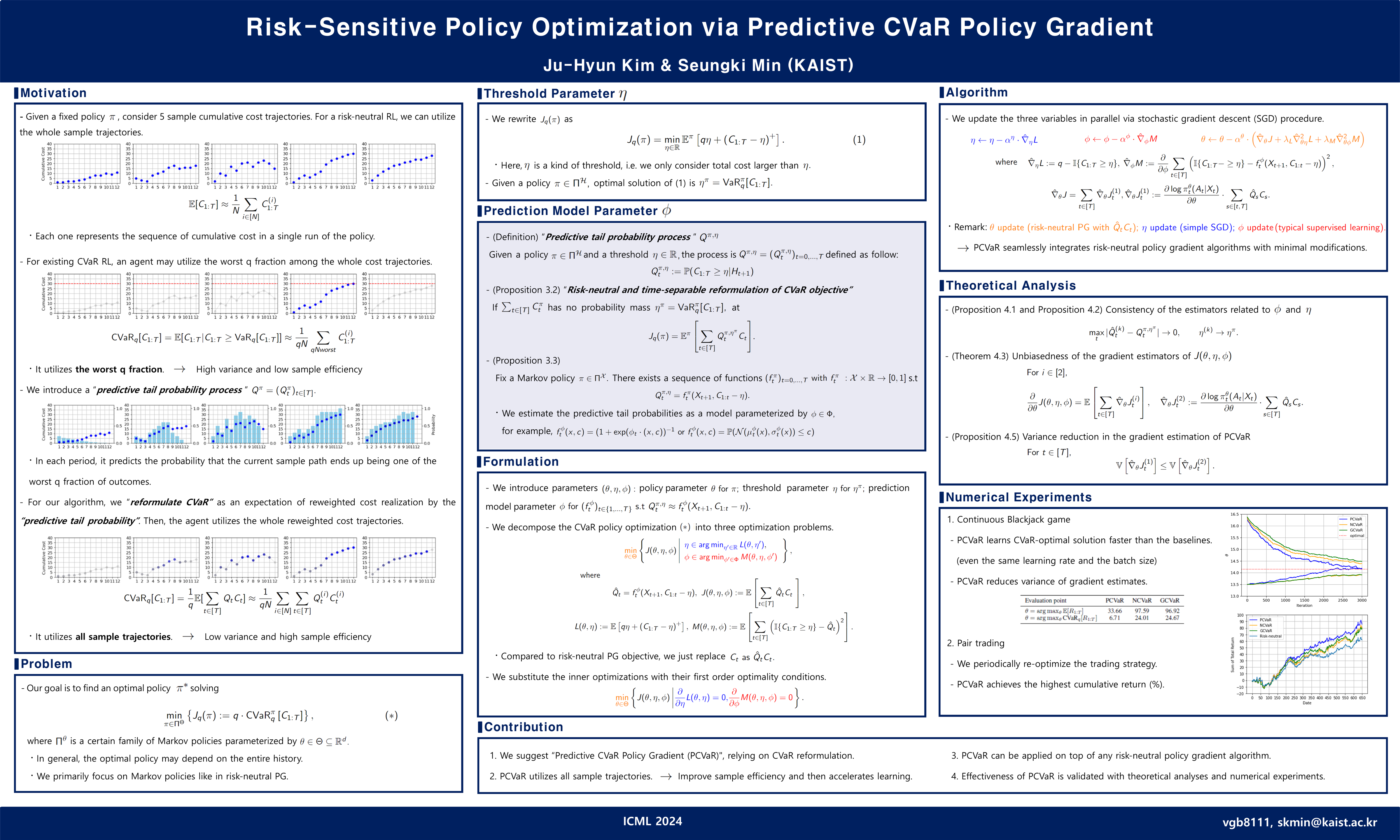

Abstract

This paper addresses a policy optimization task with the conditional value-at-risk (CVaR) objective. We introduce the predictive CVaR policy gradient, a novel approach that seamlessly integrates risk-neutral policy gradient algorithms with minimal modifications. Our method incorporates a reweighting strategy in gradient calculation -- individual cost terms are reweighted in proportion to their predicted contribution to the objective. These weights can be easily estimated through a separate learning procedure. We provide theoretical and empirical analyses, demonstrating the validity and effectiveness of our proposed method.

Chat is not available.

Successful Page Load