Autonomous Sparse Mean-CVaR Portfolio Optimization

Yizun Lin ⋅ Yangyu Zhang ⋅ Zhao-Rong Lai ⋅ Cheng Li

2024 Poster

{kind=link}

Abstract

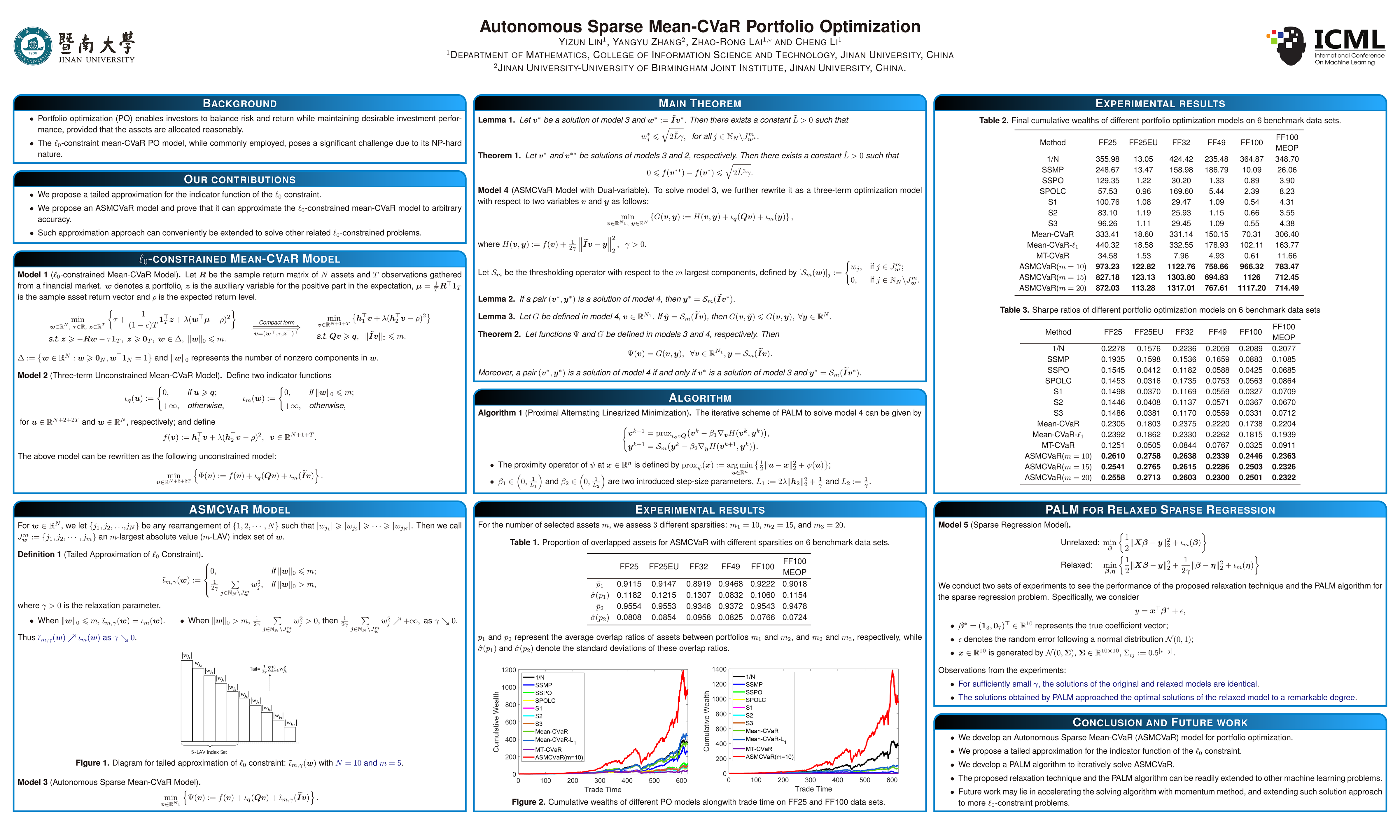

The $\ell_0$-constrained mean-CVaR model poses a significant challenge due to its NP-hard nature, typically tackled through combinatorial methods characterized by high computational demands. From a markedly different perspective, we propose an innovative autonomous sparse mean-CVaR portfolio model, capable of approximating the original $\ell_0$-constrained mean-CVaR model with arbitrary accuracy. The core idea is to convert the $\ell_0$ constraint into an indicator function and subsequently handle it through a tailed approximation. We then propose a proximal alternating linearized minimization algorithm, coupled with a nested fixed-point proximity algorithm (both convergent), to iteratively solve the model. Autonomy in sparsity refers to retaining a significant portion of assets within the selected asset pool during adjustments in pool size. Consequently, our framework offers a theoretically guaranteed approximation of the $\ell_0$-constrained mean-CVaR model, improving computational efficiency while providing a robust asset selection scheme.

Chat is not available.

Successful Page Load