Decoupling Learning and Decision-Making: Breaking the $\mathcal{O}(\sqrt{T})$ Barrier in Online Resource Allocation with First-Order Methods

Wenzhi Gao ⋅ Chunlin Sun ⋅ Chenyu Xue ⋅ Yinyu Ye

2024 Poster

{kind=link}

Abstract

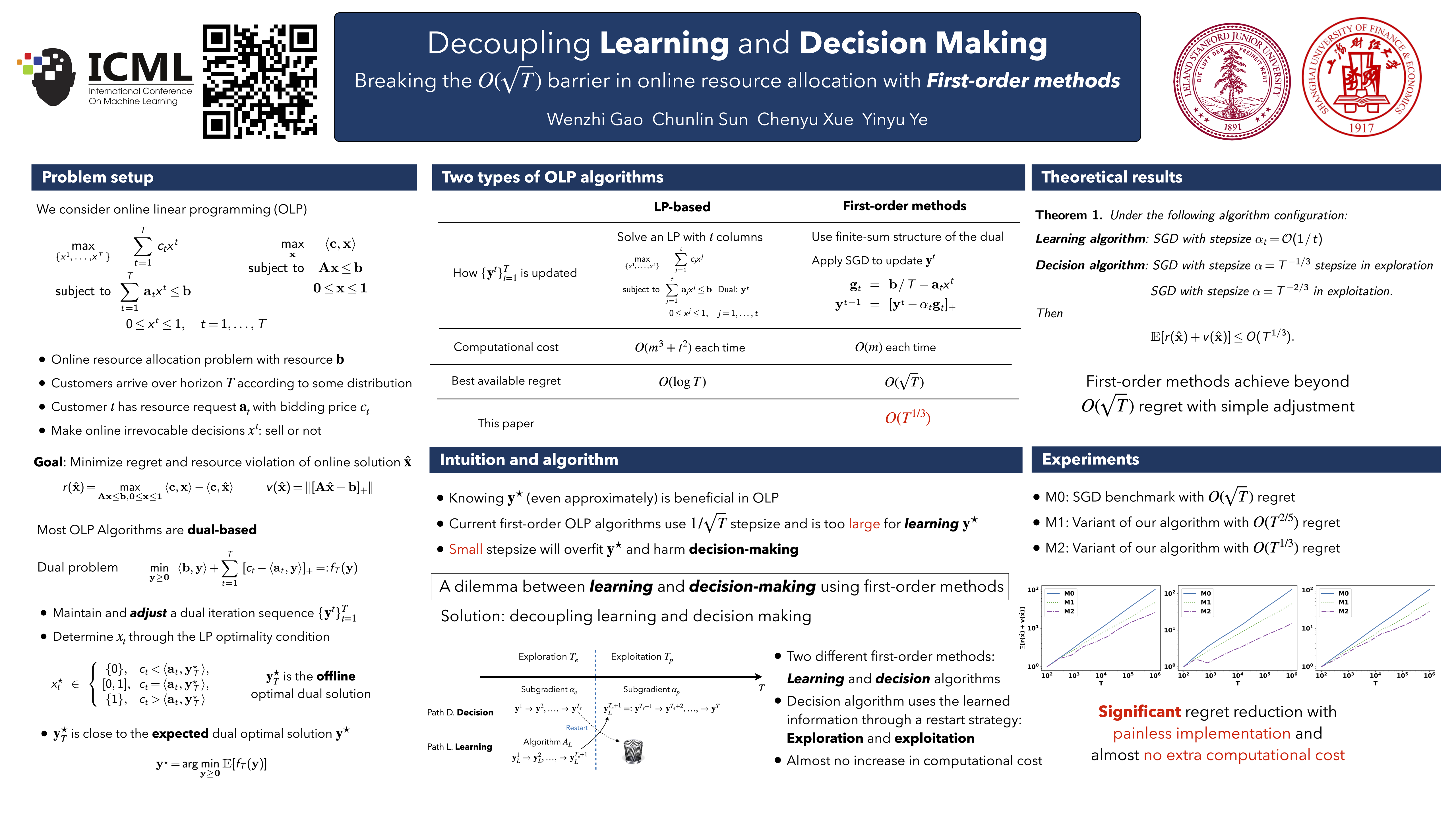

Online linear programming plays an important role in both revenue management and resource allocation, and recent research has focused on developing efficient first-order online learning algorithms. Despite the empirical success of first-order methods, they typically achieve regret no better than $\mathcal{O}(\sqrt{T})$, which is suboptimal compared to the $\mathcal{O}(\log T)$ result guaranteed by the state-of-the-art linear programming (LP)-based online algorithms. This paper establishes several important facts about online linear programming, which unveils the challenge for first-order online algorithms to achieve beyond $\mathcal{O}(\sqrt{T})$ regret. To address this challenge, we introduce a new algorithmic framework which decouples learning from decision-making. For the first time, we show that first-order methods can achieve regret $\mathcal{O}(T^{1/3})$ with this new framework.

Chat is not available.

Successful Page Load