Differentially Private Stochastic Convex Optimization under a Quantile Loss Function

Du Chen ⋅ Geoffrey Chua

2023 Poster

{kind=link}

Abstract

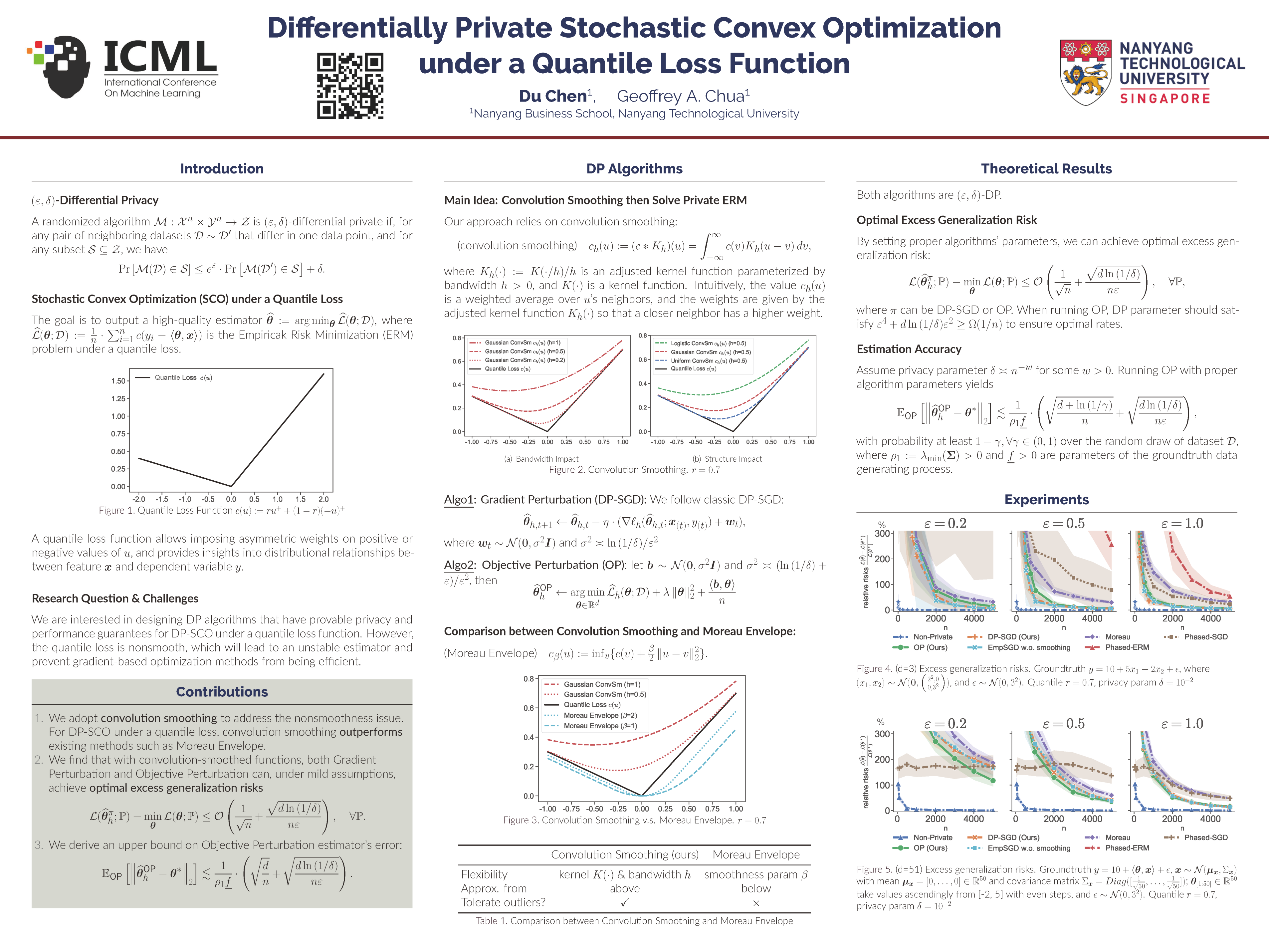

We study $(\varepsilon,\delta)$-differentially private (DP) stochastic convex optimization under an $r$-th quantile loss function taking the form $c(u) = ru^+ + (1-r)(-u)^+$. The function is non-smooth, and we propose to approximate it with a smooth function obtained by convolution smoothing, which enjoys both structure and bandwidth flexibility and can address outliers. This leads to a better approximation than those obtained from existing methods such as Moreau Envelope. We then design private algorithms based on DP stochastic gradient descent and objective perturbation, and show that both algorithms achieve (near) optimal excess generalization risk $O(\max\{\frac{1}{\sqrt{n}}, \frac{\sqrt{d\ln(1/\delta)}}{n\varepsilon}\})$. Through objective perturbation, we further derive an upper bound $O(\max\{\sqrt{\frac{d}{n}}, \sqrt{\frac{d\ln(1/\delta)}{n\varepsilon}}\})$ on the parameter estimation error under mild assumptions on data generating processes. Some applications in private quantile regression and private inventory control will be discussed.

Video

Chat is not available.

Successful Page Load