Semi-Parametric Contextual Pricing Algorithm using Cox Proportional Hazards Model

Young-Geun Choi ⋅ Gi-Soo Kim ⋅ Choi Yunseo ⋅ Wooseong Cho ⋅ Myunghee Cho Paik ⋅ Min-hwan Oh

2023 Poster

{kind=link}

Abstract

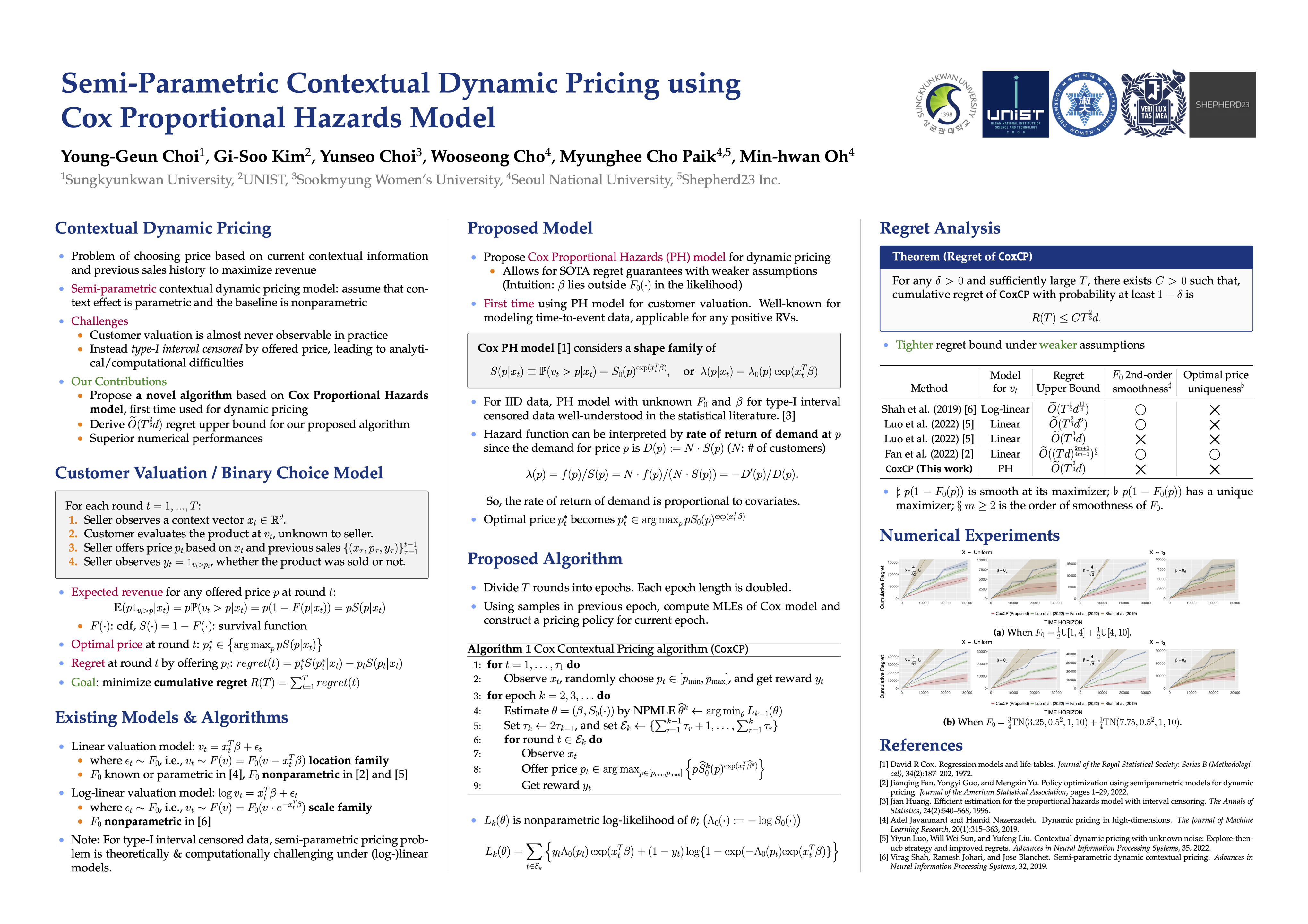

Contextual dynamic pricing is a problem of setting prices based on current contextual information and previous sales history to maximize revenue. A popular approach is to postulate a distribution of customer valuation as a function of contextual information and the baseline valuation. A semi-parametric setting, where the context effect is parametric and the baseline is nonparametric, is of growing interest due to its flexibility. A challenge is that customer valuation is almost never observable in practice and is instead *type-I interval censored* by the offered price. To address this challenge, we propose a novel semi-parametric contextual pricing algorithm for stochastic contexts, called the epoch-based Cox proportional hazards Contextual Pricing (CoxCP) algorithm. To our best knowledge, our work is the first to employ the Cox model for customer valuation. The CoxCP algorithm has a high-probability regret upper bound of $\tilde{O}( T^{\frac{2}{3}}d )$, where $T$ is the length of horizon and $d$ is the dimension of context. In addition, if the baseline is known, the regret bound can improve to $O( d \log T )$ under certain assumptions. We demonstrate empirically the proposed algorithm performs better than existing semi-parametric contextual pricing algorithms when the model assumptions of all algorithms are correct.

Video

Chat is not available.

Successful Page Load