Multicalibration as Boosting for Regression

Ira Globus-Harris ⋅ Declan Harrison ⋅ Michael Kearns ⋅ Aaron Roth ⋅ Jessica Sorrell

2023 Poster

{kind=link}

Abstract

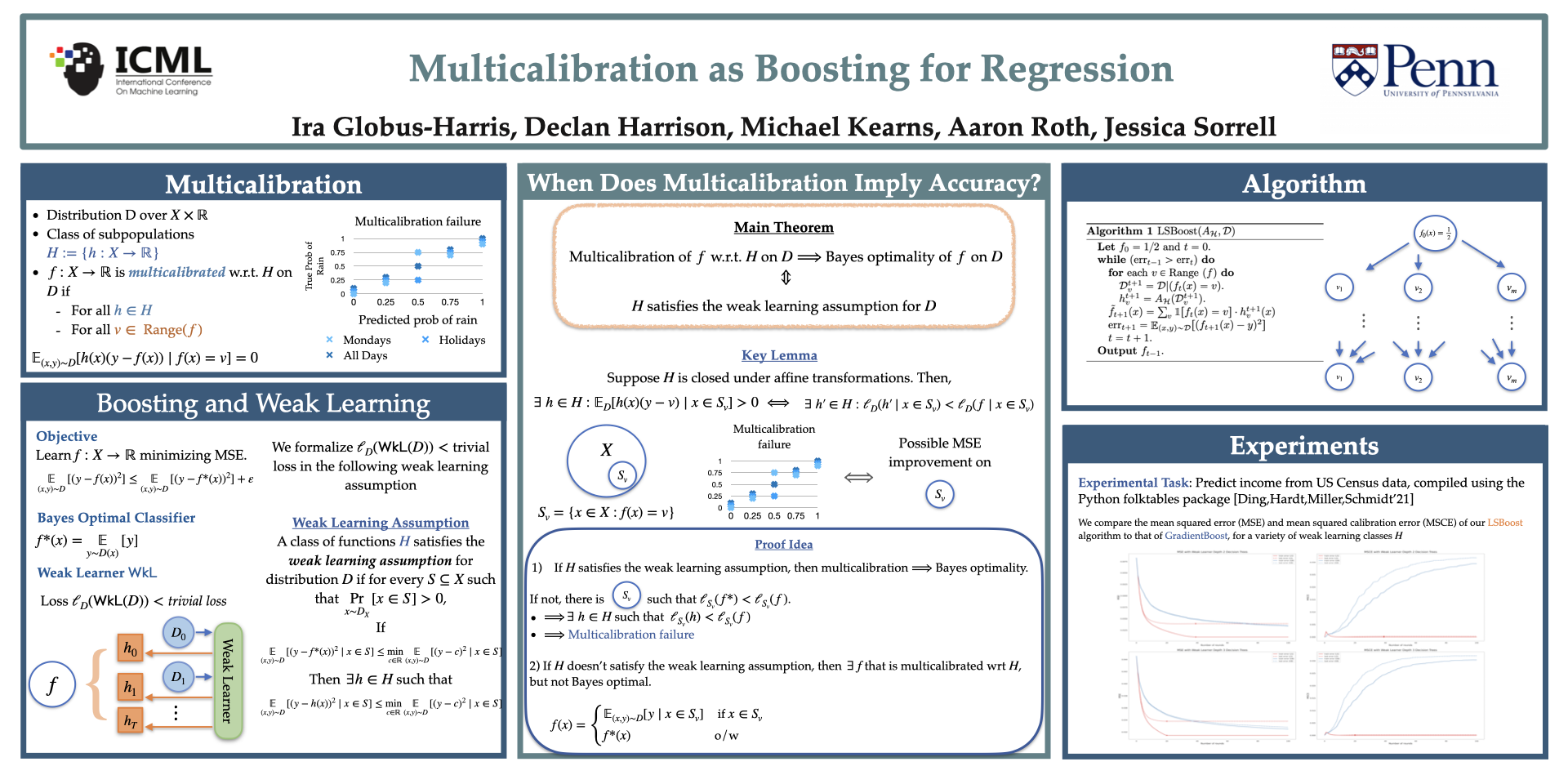

We study the connection between multicalibration and boosting for squared error regression. First we prove a useful characterization of multicalibration in terms of a ``swap regret'' like condition on squared error. Using this characterization, we give an exceedingly simple algorithm that can be analyzed both as a boosting algorithm for regression and as a multicalibration algorithm for a class $\mathcal{H}$ that makes use only of a standard squared error regression oracle for $\mathcal{H}$. We give a weak learning assumption on $\mathcal{H}$ that ensures convergence to Bayes optimality without the need to make any realizability assumptions --- giving us an agnostic boosting algorithm for regression. We then show that our weak learning assumption on $\mathcal{H}$ is both necessary and sufficient for multicalibration with respect to $\mathcal{H}$ to imply Bayes optimality, answering an open question. We also show that if $\mathcal{H}$ satisfies our weak learning condition relative to another class $\mathcal{C}$ then multicalibration with respect to $\mathcal{H}$ implies multicalibration with respect to $\mathcal{C}$. Finally we investigate the empirical performance of our algorithm experimentally.

Video

Chat is not available.

Successful Page Load