Extending Conformal Prediction to Hidden Markov Models with Exact Validity via de Finetti's Theorem for Markov Chains

{kind=link}

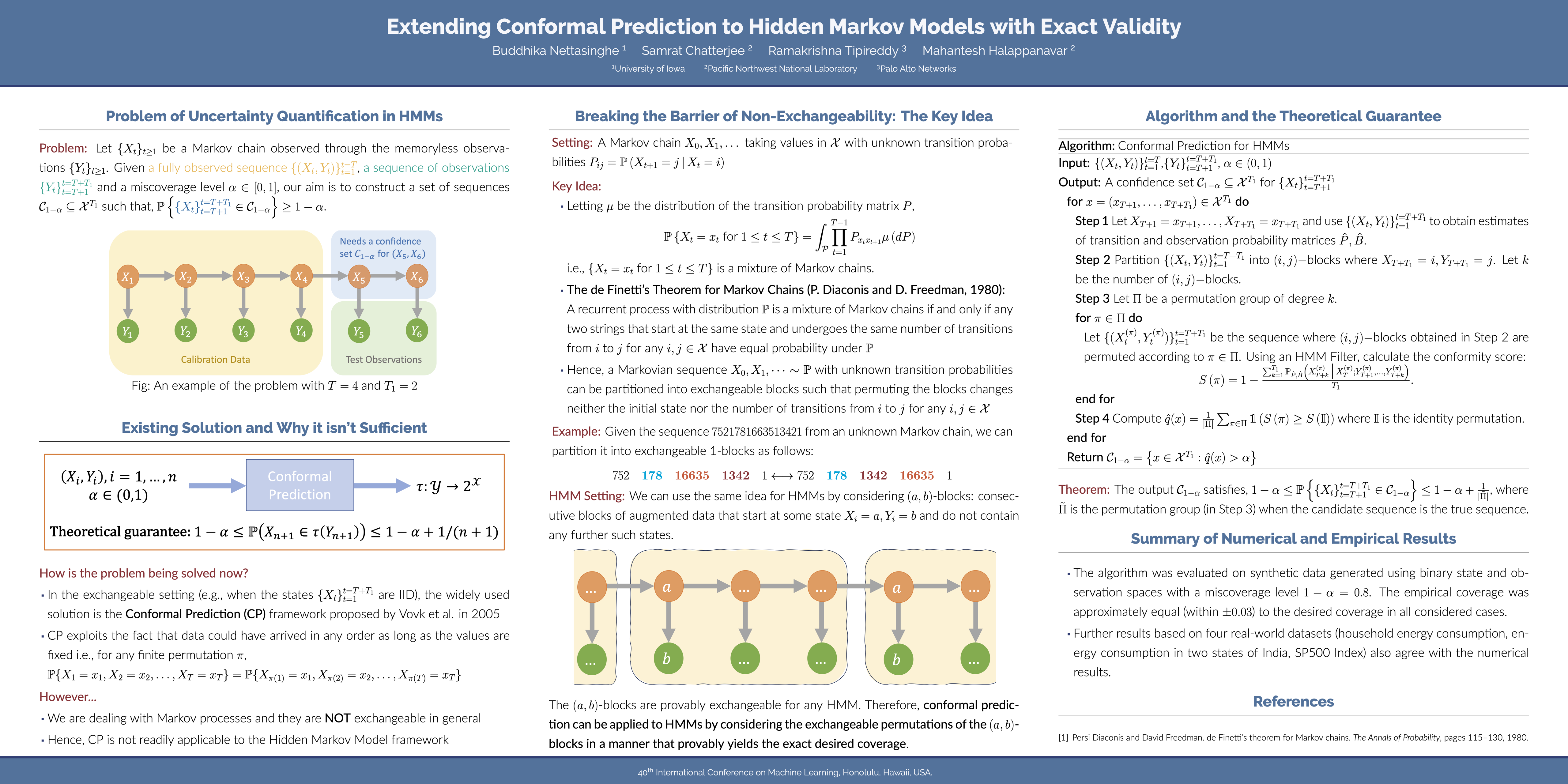

Abstract

Conformal prediction is a widely used method to quantify the uncertainty of a classifier under the assumption of exchangeability (e.g., IID data). We generalize conformal prediction to the Hidden Markov Model (HMM) framework where the assumption of exchangeability is not valid. The key idea of the proposed method is to partition the non-exchangeable Markovian data from the HMM into exchangeable blocks by exploiting the de Finetti's Theorem for Markov Chains discovered by Diaconis and Freedman (1980). The permutations of the exchangeable blocks are viewed as randomizations of the observed Markovian data from the HMM. The proposed method provably retains all desirable theoretical guarantees offered by the classical conformal prediction framework in both exchangeable and Markovian settings. In particular, while the lack of exchangeability introduced by Markovian samples constitutes a violation of a crucial assumption for classical conformal prediction, the proposed method views it as an advantage that can be exploited to improve the performance further. Detailed numerical and empirical results that complement the theoretical conclusions are provided to illustrate the practical feasibility of the proposed method.