Machine learning over the free-parameters of the Black-Scholes equation: Stock market and Option market

JORGE ARRAUT ⋅ Ivan Arraut ⋅ Ka I Lei

2023 Poster

in

Affinity Event: LatinX in AI (LXAI) Workshop

in

Affinity Event: LatinX in AI (LXAI) Workshop

{kind=link}

Abstract

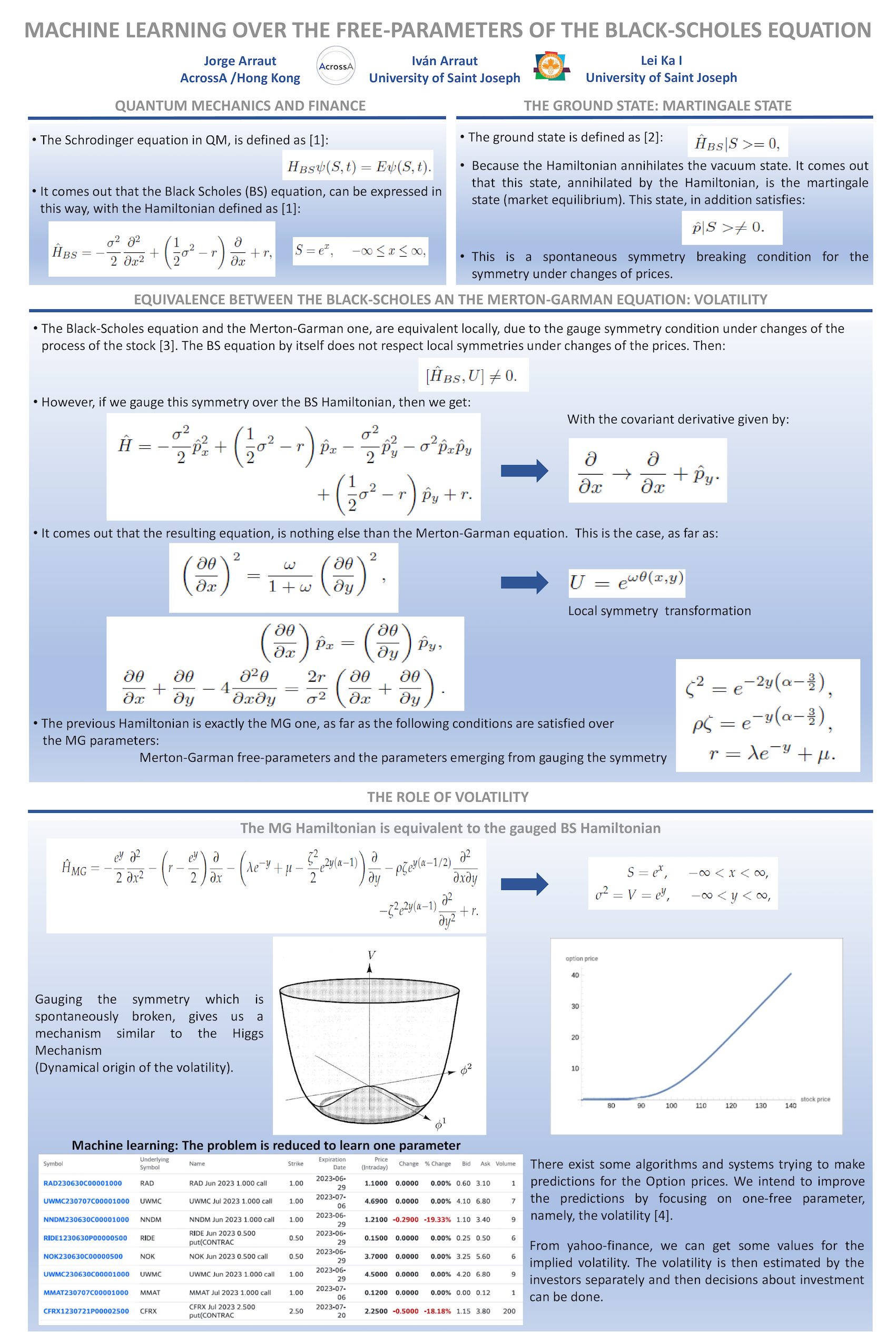

The Black-Scholes equation is famous for predictingvalues for the prices of Options inside thestock market scenario. However, it has the limitationof depending on the estimated value forthe volatility. On the other hand, several Machinelearning techniques have been employed for predictingthe values of the same quantity. In thispaper we analyze some fundamental properties ofthe Black-Scholes equation and we then proposea way to train its free-parameters, the volatilityin particular. This with the purpose of using thisparameter as the fundamental one to be learnedby a Machine Learning system and then improvethe predictions in the stock market.

Video

Chat is not available.

Successful Page Load