Adaptive Conformal Predictions for Time Series

{kind=link}

Abstract

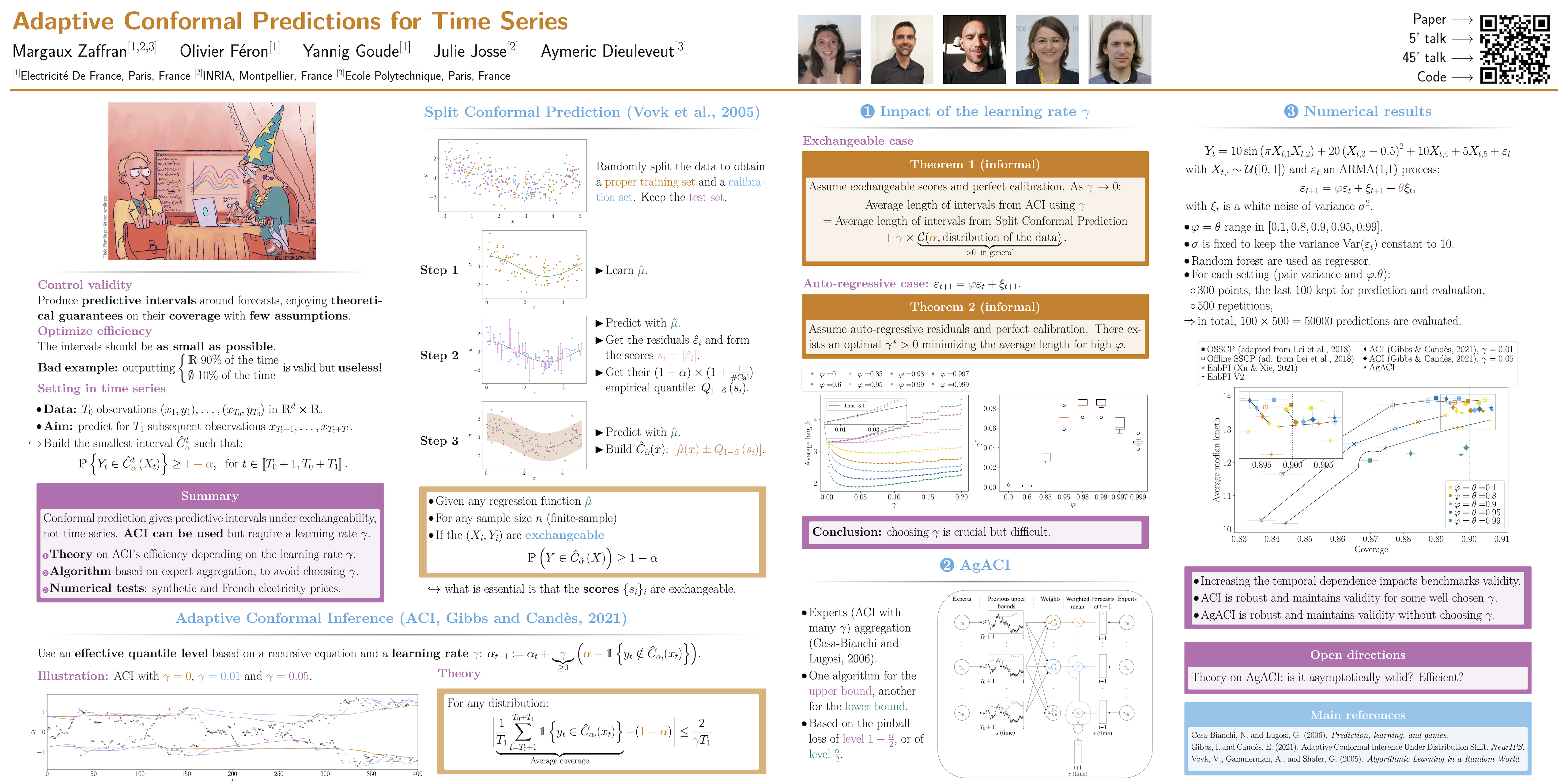

Uncertainty quantification of predictive models is crucial in decision-making problems. Conformal prediction is a general and theoretically sound answer. However, it requires exchangeable data, excluding time series. While recent works tackled this issue, we argue that Adaptive Conformal Inference (ACI, Gibbs & Candès, 2021), developed for distribution-shift time series, is a good procedure for time series with general dependency. We theoretically analyse the impact of the learning rate on its efficiency in the exchangeable and auto-regressive case. We propose a parameter-free method, AgACI, that adaptively builds upon ACI based on online expert aggregation. We lead extensive fair simulations against competing methods that advocate for ACI's use in time series. We conduct a real case study: electricity price forecasting. The proposed aggregation algorithm provides efficient prediction intervals for day-ahead forecasting. All the code and data to reproduce the experiments are made available on GitHub.