Online Learning and Pricing with Reusable Resources: Linear Bandits with Sub-Exponential Rewards

Huiwen Jia ⋅ Cong Shi ⋅ Siqian Shen

2022 Poster

{kind=link}

Abstract

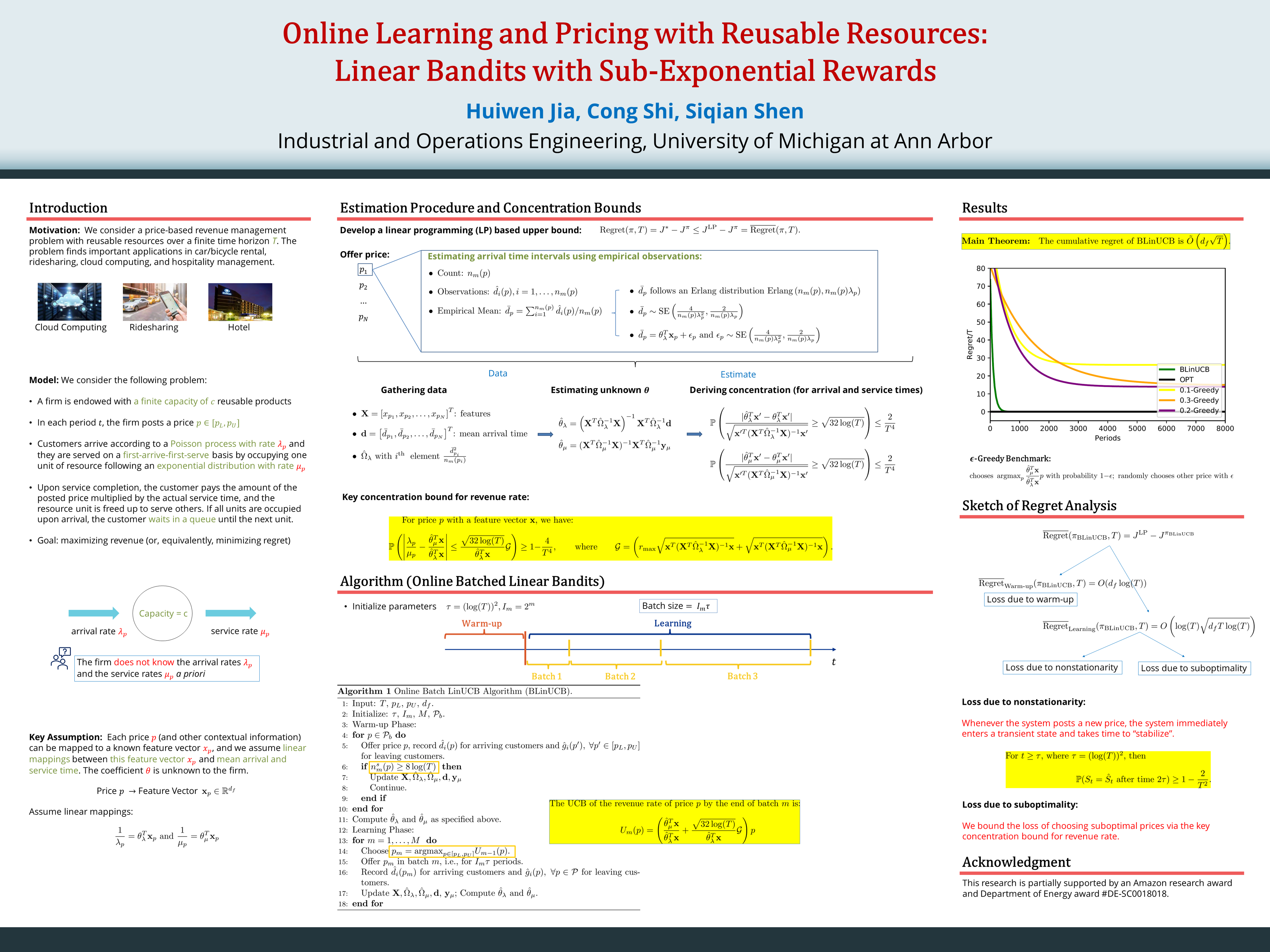

We consider a price-based revenue management problem with reusable resources over a finite time horizon $T$. The problem finds important applications in car/bicycle rental, ridesharing, cloud computing, and hospitality management. Customers arrive following a price-dependent Poisson process and each customer requests one unit of $c$ homogeneous reusable resources. If there is an available unit, the customer gets served within a price-dependent exponentially distributed service time; otherwise, she waits in a queue until the next available unit. The decision maker assumes that the inter-arrival and service intervals have an unknown linear dependence on a $d_f$-dimensional feature vector associated with the posted price. We propose a rate-optimal online learning and pricing algorithm, termed Batch Linear Confidence Bound (BLinUCB), and prove that the cumulative regret is $\tilde{O}( d_f \sqrt{T } )$. In establishing the regret, we bound the transient system performance upon price changes via a coupling argument, and also generalize linear bandits to accommodate sub-exponential rewards.

Chat is not available.

Successful Page Load