Sequential Monte Carlo Learning for Time Series Structure Discovery

{kind=link}

Abstract

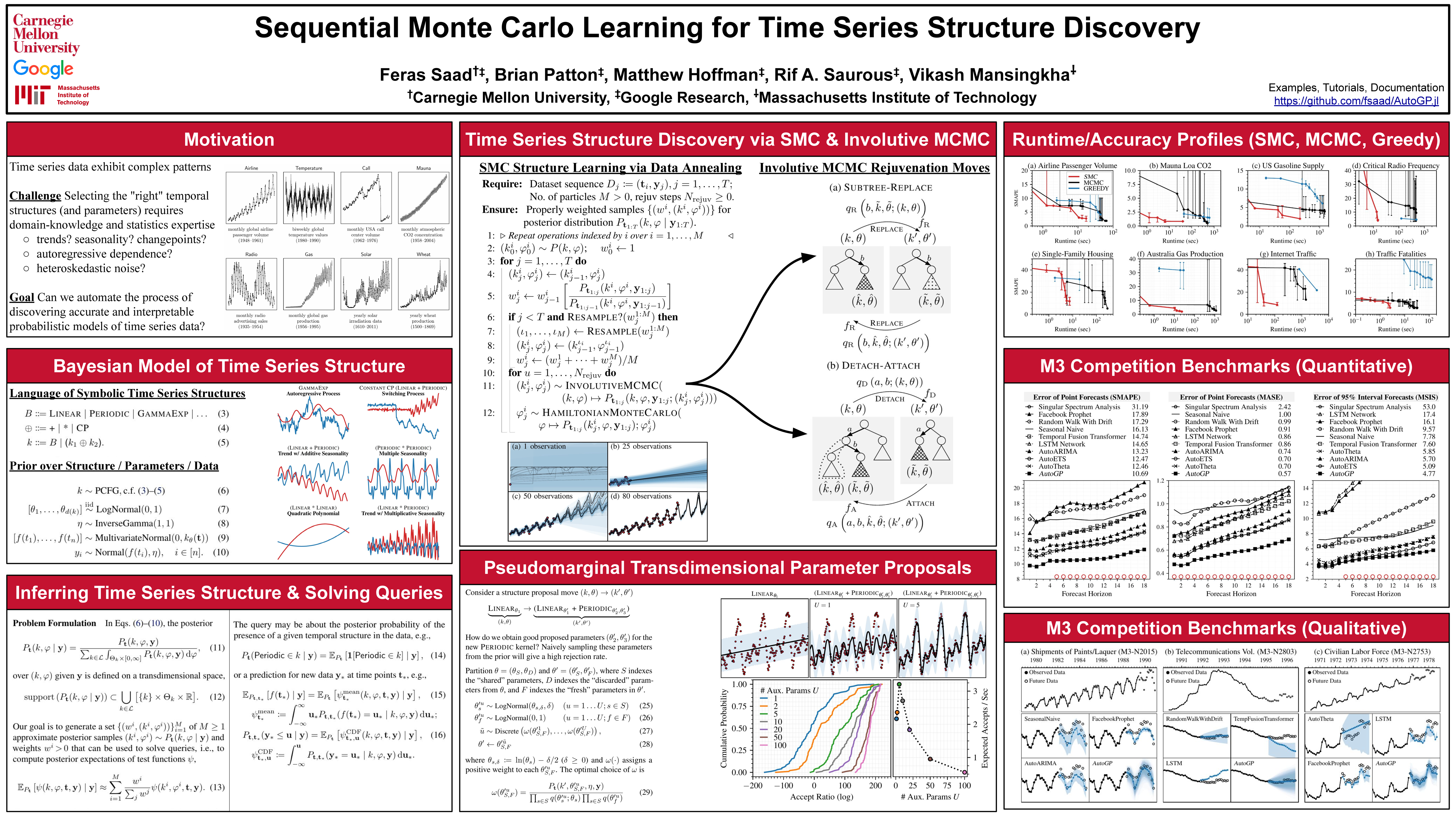

This paper presents a new approach to automatically discovering accurate models of complex time series data. Working within a Bayesian nonparametric prior over a symbolic space of Gaussian process time series models, we present a novel structure learning algorithm that integrates sequential Monte Carlo (SMC) and involutive MCMC for highly effective posterior inference. Our method can be used both in "online'' settings, where new data is incorporated sequentially in time, and in ``offline'' settings, by using nested subsets of historical data to anneal the posterior. Empirical measurements on real-world time series show that our method can deliver 10x--100x runtime speedups over previous MCMC and greedy-search structure learning algorithms targeting the same model family. We use our method to perform the first large-scale evaluation of Gaussian process time series structure learning on a prominent benchmark of 1,428 econometric datasets. The results show that our method discovers sensible models that deliver more accurate point forecasts and interval forecasts over multiple horizons as compared to widely used statistical and neural baselines that struggle on this challenging data.