Robust and Scalable Bayesian Online Changepoint Detection

Matias Altamirano ⋅ Francois-Xavier Briol ⋅ Jeremias Knoblauch

2023 Poster

{kind=link}

Abstract

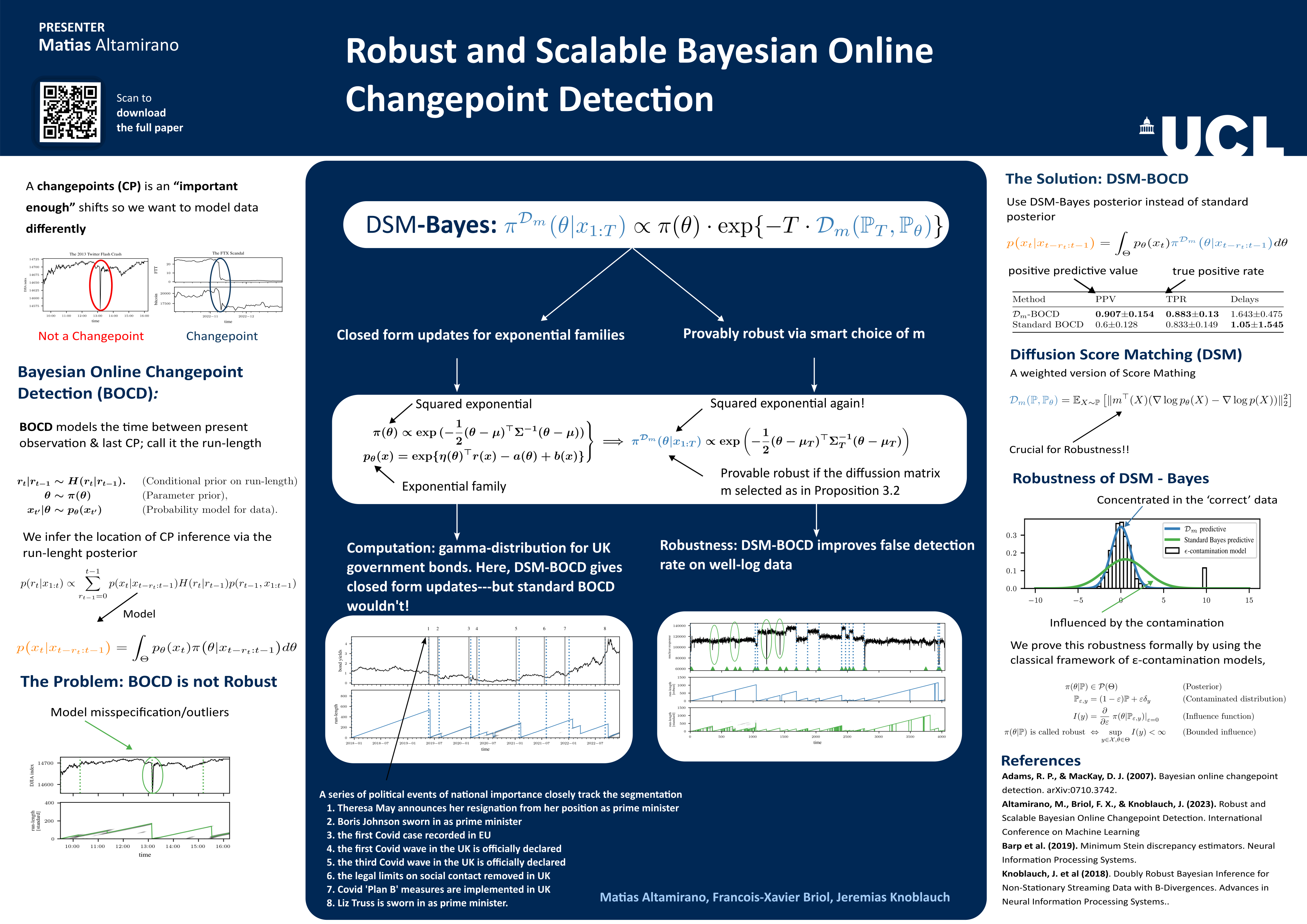

This paper proposes an online, provably robust, and scalable Bayesian approach for changepoint detection. The resulting algorithm has key advantages over previous work: it provides provable robustness by leveraging the generalised Bayesian perspective, and also addresses the scalability issues of previous attempts. Specifically, the proposed generalised Bayesian formalism leads to conjugate posteriors whose parameters are available in closed form by leveraging diffusion score matching. The resulting algorithm is exact, can be updated through simple algebra, and is more than 10 times faster than its closest competitor.

Video

Chat is not available.

Successful Page Load