Optimal No-Regret Learning for One-Sided Lipschitz Functions

PAUL DUETTING ⋅ Guru Guruganesh ⋅ Jon Schneider ⋅ Joshua Wang

2023 Poster

{kind=link}

Abstract

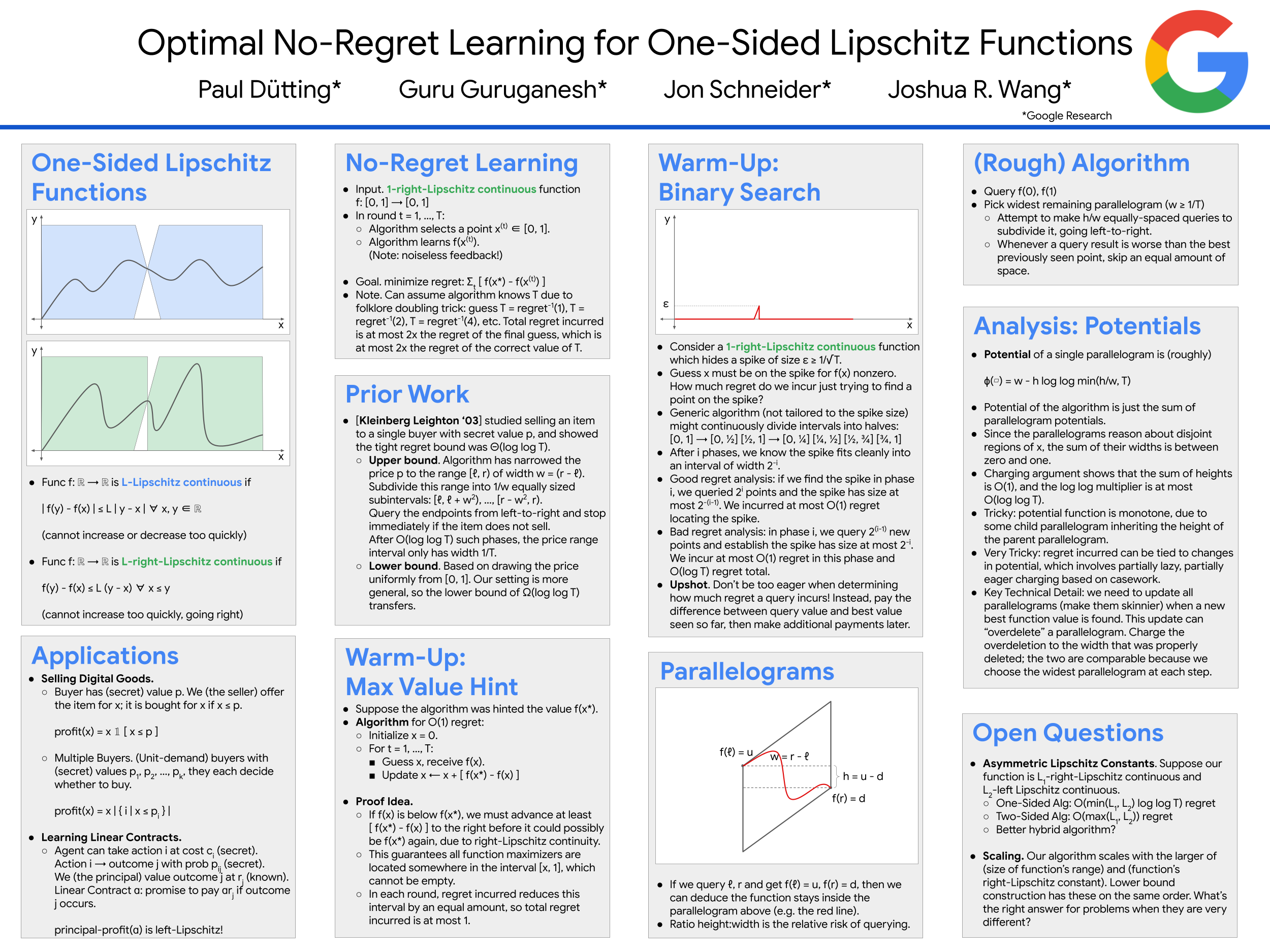

Inspired by applications in pricing and contract design, we study the maximization of one-sided Lipschitz functions, which only provide the (weaker) guarantee that they do not grow too quickly in one direction. We show that it is possible to learn a maximizer for such a function while incurring $O(\log \log T)$ total regret (with a universal constant independent of the number of discontinuities / complexity of the function). This regret bound is asymptotically optimal in $T$ due to a lower bound of Kleinberg and Leighton. By applying this algorithm, we show that one can sell digital goods to multiple buyers and learn the optimal linear contract in the principal-agent setting while incurring at most $O(\log \log T)$ regret.

Video

Chat is not available.

Successful Page Load