Modeling Temporal Data as Continuous Functions with Stochastic Process Diffusion

{kind=link}

Abstract

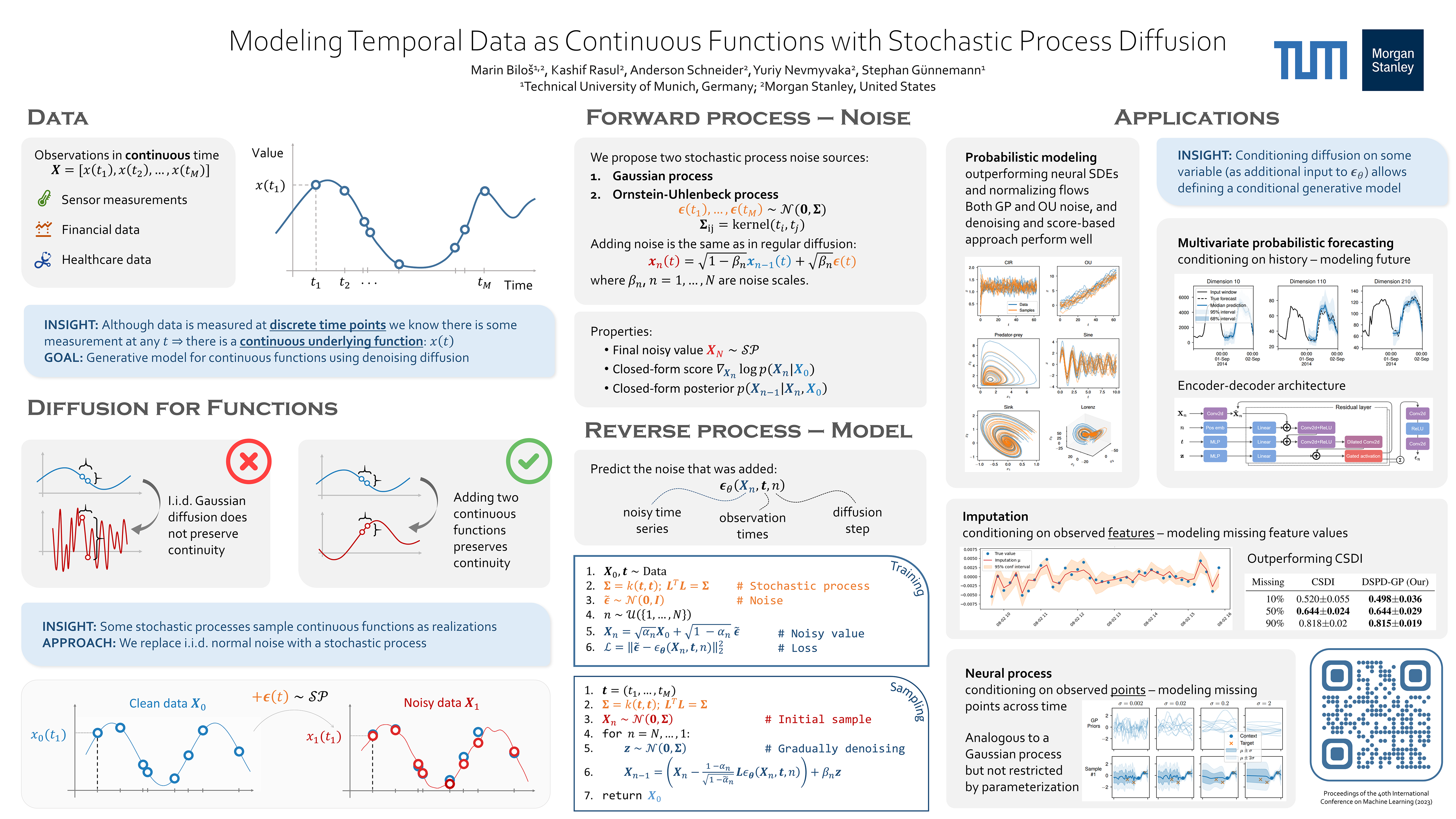

Temporal data such as time series can be viewed as discretized measurements of the underlying function. To build a generative model for such data we have to model the stochastic process that governs it. We propose a solution by defining the denoising diffusion model in the function space which also allows us to naturally handle irregularly-sampled observations. The forward process gradually adds noise to functions, preserving their continuity, while the learned reverse process removes the noise and returns functions as new samples. To this end, we define suitable noise sources and introduce novel denoising and score-matching models. We show how our method can be used for multivariate probabilistic forecasting and imputation, and how our model can be interpreted as a neural process.