A Model-Based Method for Minimizing CVaR and Beyond

{kind=link}

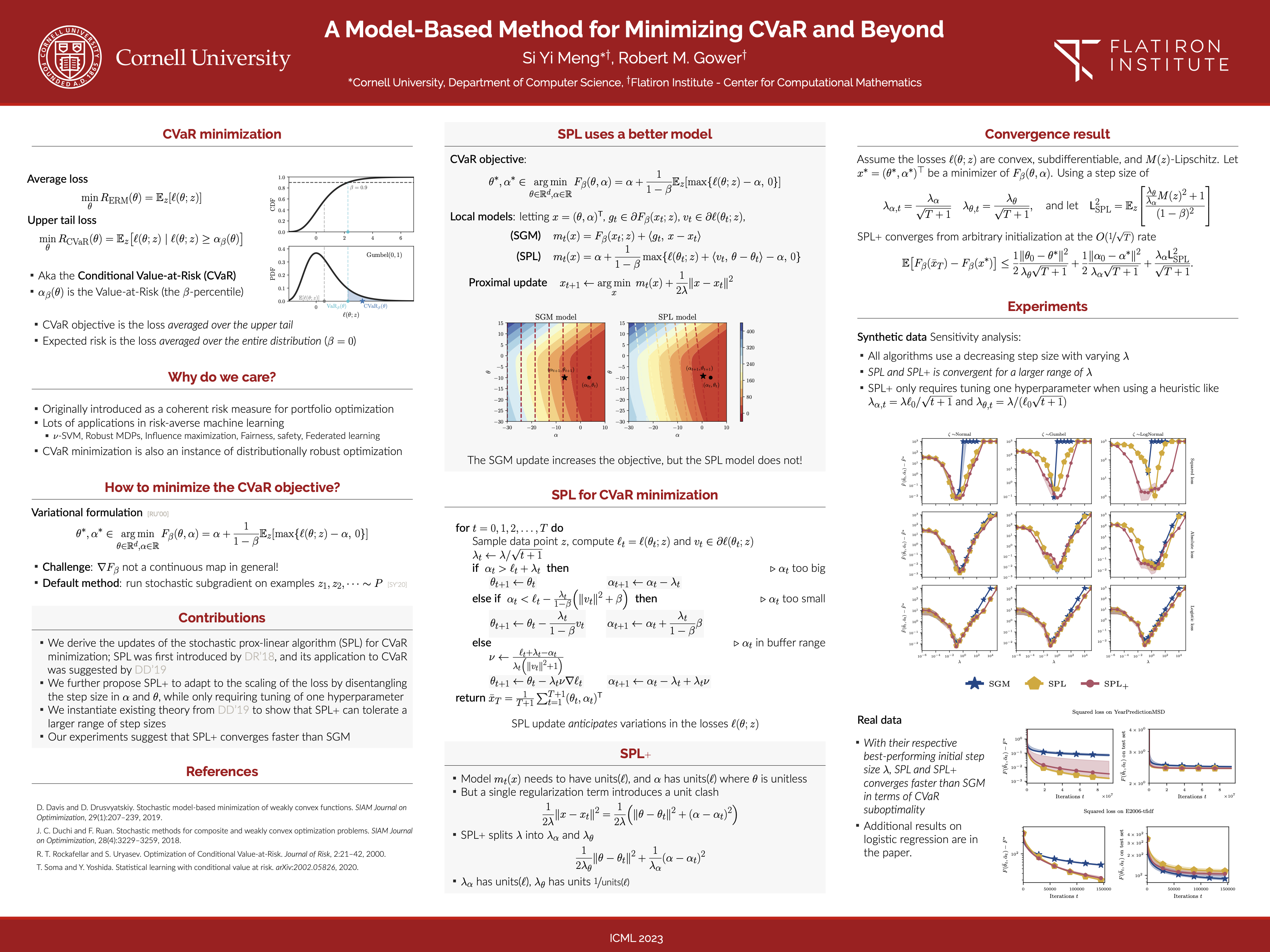

Abstract

We develop a variant of the stochastic prox-linear method for minimizing the Conditional Value-at-Risk (CVaR) objective. CVaR is a risk measure focused on minimizing worst-case performance, defined as the average of the top quantile of the losses. In machine learning, such a risk measure is useful to train more robust models. Although the stochastic subgradient method (SGM) is a natural choice for minimizing the CVaR objective, we show that our stochastic prox-linear (SPL+) algorithm can better exploit the structure of the objective, while still providing a convenient closed form update. Our SPL+ method also adapts to the scaling of the loss function, which allows for easier tuning. We then specialize a general convergence theorem for SPL+ to our setting, and show that it allows for a wider selection of step sizes compared to SGM. We support this theoretical finding experimentally.