Revisiting Online Submodular Minimization: Gap-Dependent Regret Bounds, Best of Both Worlds and Adversarial Robustness

Shinji Ito

Keywords:

OPT: Non-Convex

OPT: Discrete and Combinatorial Optimization

T: Online Learning and Bandits

2022 Poster

{kind=link}

Abstract

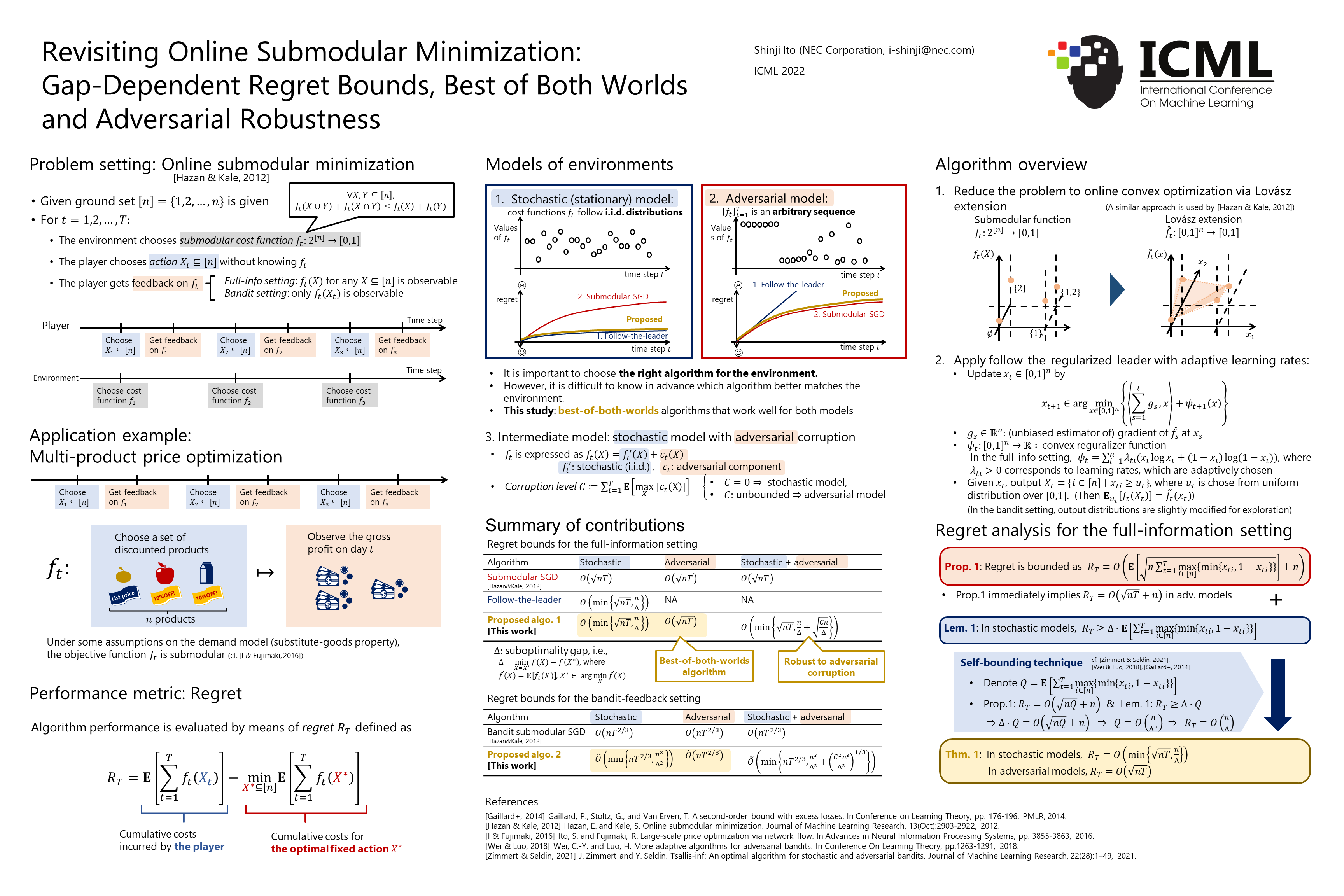

In this paper, we consider online decision problems with submodular loss functions. For such problems, existing studies have only dealt with worst-case analysis. This study goes beyond worst-case analysis to show instance-dependent regret bounds. More precisely, for each of the full-information and bandit-feedback settings, we propose an algorithm that achieves a gap-dependent O(log T)-regret bound in the stochastic environment and is comparable to the best existing algorithm in the adversarial environment. The proposed algorithms also work well in the stochastic environment with adversarial corruptions, which is an intermediate setting between the stochastic and adversarial environments.

Chat is not available.

Successful Page Load