Least Squares Estimation using Sketched Data with Heteroskedastic Errors

{kind=link}

Abstract

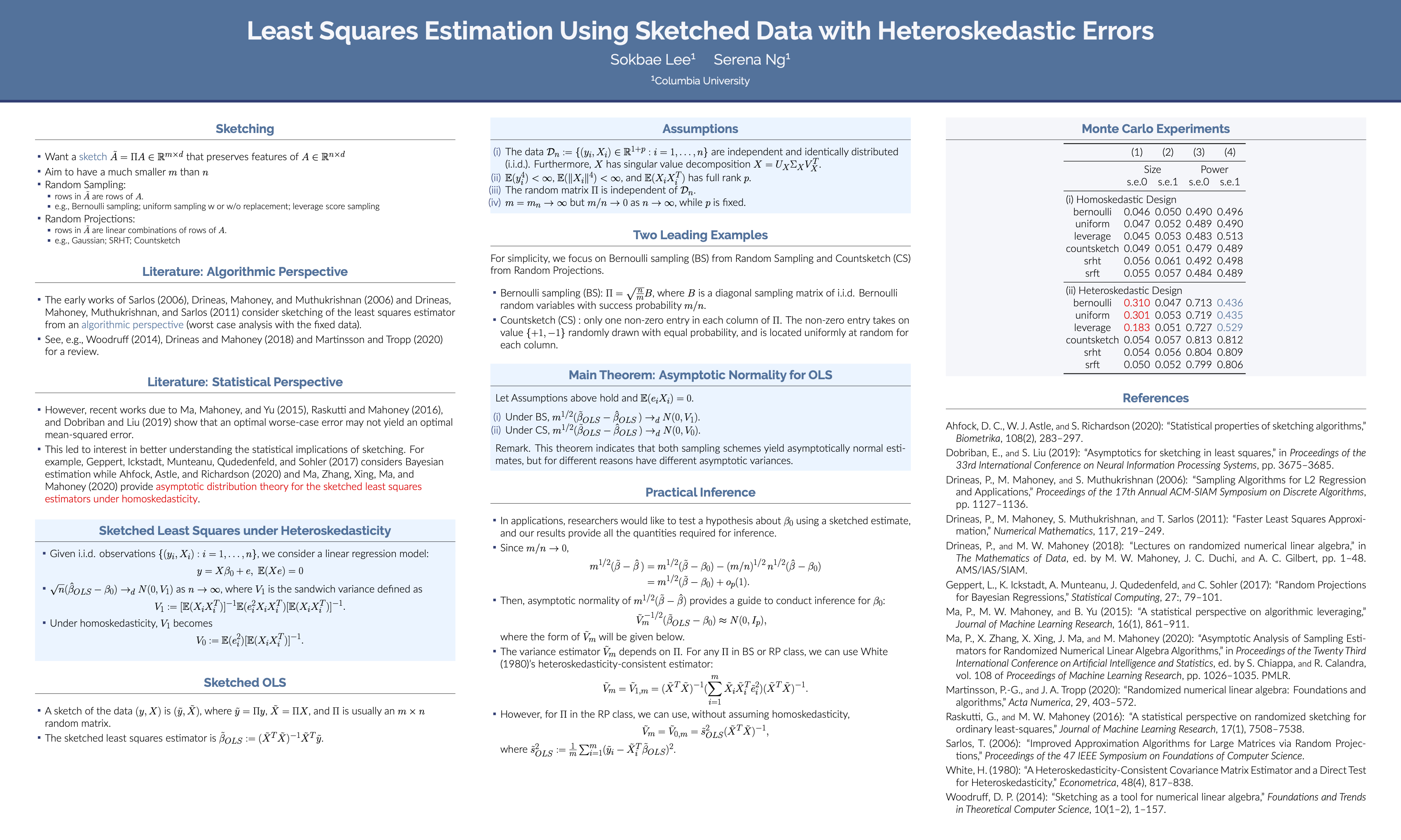

Researchers may perform regressions using a sketch of data of size m instead of the full sample of size n for a variety of reasons. This paper considers the case when the regression errors do not have constant variance and heteroskedasticity robust standard errors would normally be needed for test statistics to provide accurate inference. We show that estimates using data sketched by random projections will behave 'as if' the errors were homoskedastic. Estimation by random sampling would not have this property. The result arises because the sketched estimates in the case of random projections can be expressed as degenerate U-statistics, and under certain conditions, these statistics are asymptotically normal with homoskedastic variance. We verify that the conditions hold not only in the case of least squares regression when the covariates are exogenous, but also in instrumental variables estimation when the covariates are endogenous. The result implies that inference can be simpler than the full sample case if the sketching scheme is appropriately chosen.