Minimax Classification under Concept Drift with Multidimensional Adaptation and Performance Guarantees

{kind=link}

Abstract

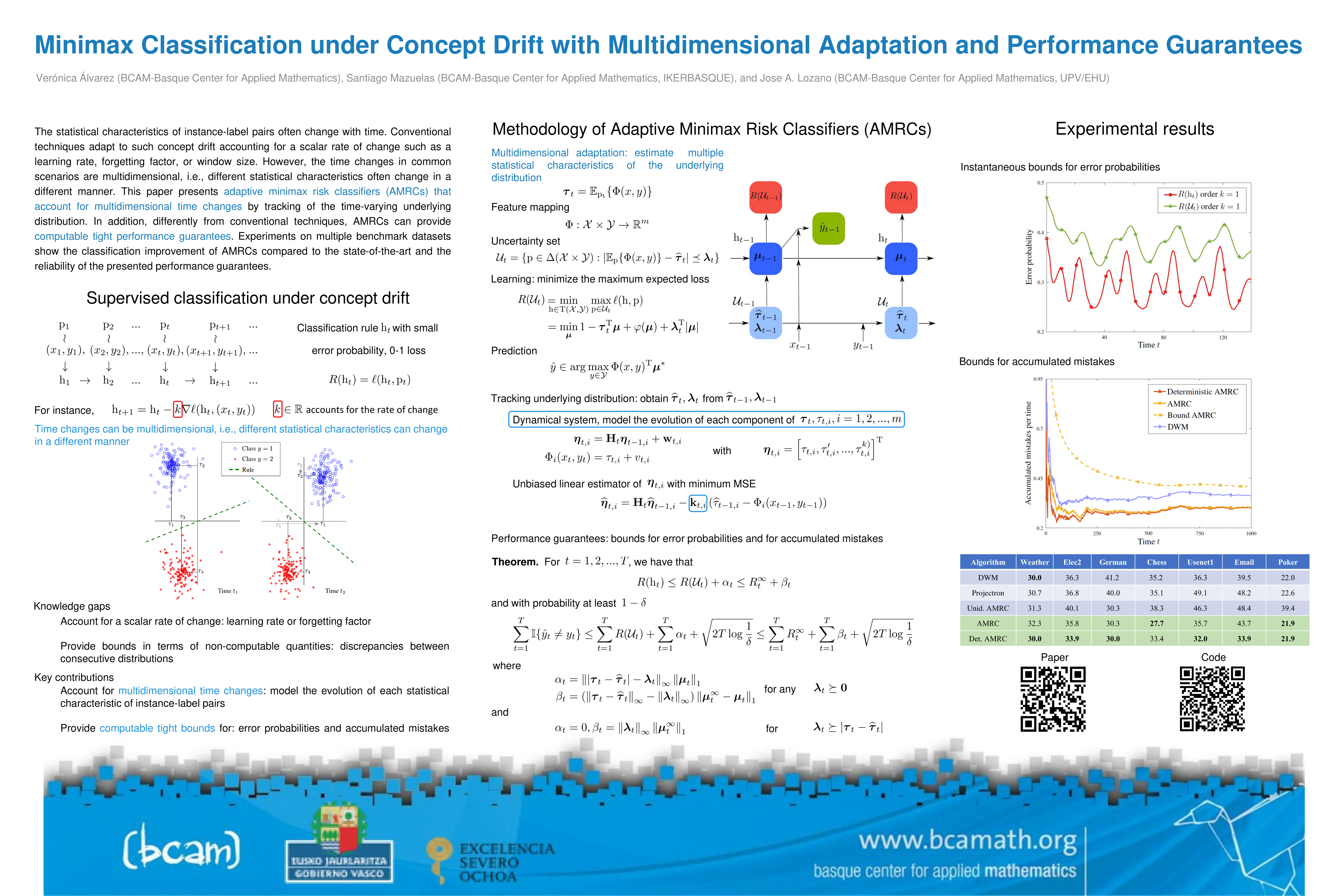

The statistical characteristics of instance-label pairs often change with time in practical scenarios of supervised classification. Conventional learning techniques adapt to such concept drift accounting for a scalar rate of change by means of a carefully chosen learning rate, forgetting factor, or window size. However, the time changes in common scenarios are multidimensional, i.e., different statistical characteristics often change in a different manner. This paper presents adaptive minimax risk classifiers (AMRCs) that account for multidimensional time changes by means of a multivariate and high-order tracking of the time-varying underlying distribution. In addition, differently from conventional techniques, AMRCs can provide computable tight performance guarantees. Experiments on multiple benchmark datasets show the classification improvement of AMRCs compared to the state-of-the-art and the reliability of the presented performance guarantees.