machine learning

-

Shike Mei and Jun Zhu and Jerry Zhu

Robust RegBayes: Selectively Incorporating First-Order Logic Domain Knowledge into Bayesian Models (pdf)

Much research in Bayesian modeling has been done to elicit a prior distribution that incorporates domain knowledge. We present a novel and more direct approach by imposing First-Order Logic (FOL) rules on the posterior distribution. Our approach unifies FOL and Bayesian modeling under the regularized Bayesian framework. In addition, our approach automatically estimates the uncertainty of FOL rules when they are produced by humans, so that reliable rules are incorporated while unreliable ones are ignored. We apply our approach to latent topic modeling tasks and demonstrate that by combining FOL knowledge and Bayesian modeling, we both improve the task performance and discover more structured latent representations in unsupervised and supervised learning.

-

Travis Dick and Andras Gyorgy and Csaba Szepesvari

Online Learning in Markov Decision Processes with Changing Cost Sequences (pdf)

In this paper we consider online learning in finite Markov decision processes (MDPs) with changing cost sequences under full and bandit-information. We propose to view this problem as an instance of online linear optimization. We propose two methods for this problem: MD^2 (mirror descent with approximate projections) and the continuous exponential weights algorithm with Dikin walks. We provide a rigorous complexity analysis of these techniques, while providing near-optimal regret-bounds (in particular, we take into account the computational costs of performing approximate projections in MD^2). In the case of full-information feedback, our results complement existing ones. In the case of bandit-information feedback we consider the online stochastic shortest path problem, a special case of the above MDP problems, and manage to improve the existing results by removing the previous restrictive assumption that the state-visitation probabilities are uniformly bounded away from zero under all policies.

-

Stanley Chan and Edoardo Airoldi

A Consistent Histogram Estimator for Exchangeable Graph Models (pdf)

Exchangeable graph models (ExGM) subsume a number of popular network models. The mathematical object that characterizes an ExGM is termed a graphon. Finding scalable estimators of graphons, provably consistent, remains an open issue. In this paper, we propose a histogram estimator of a graphon that is provably consistent and numerically efficient. The proposed estimator is based on a sorting-and-smoothing (SAS) algorithm, which first sorts the empirical degree of a graph, then smooths the sorted graph using total variation minimization. The consistency of the SAS algorithm is proved by leveraging sparsity concepts from compressed sensing.

-

Arun Rajkumar and Shivani Agarwal

A Statistical Convergence Perspective of Algorithms for Rank Aggregation from Pairwise Data (pdf)

There has been much interest recently in the problem of rank aggregation from pairwise data. A natural question that arises is: under what sorts of statistical assumptions do various rank aggregation algorithms converge to an `optimal' ranking? In this paper, we consider this question in a natural setting where pairwise comparisons are drawn randomly and independently from some underlying probability distribution. We first show that, under a `time-reversibility' or Bradley-Terry-Luce (BTL) condition on the distribution generating the outcomes of the pairwise comparisons, the rank centrality (PageRank) and least squares (HodgeRank) algorithms both converge to an optimal ranking. Next, we show that a matrix version of the Borda count algorithm, and more surprisingly, an algorithm which performs maximal likelihood estimation under a BTL assumption, both converge to an optimal ranking under a `low-noise' condition that is strictly more general than BTL. Finally, we propose a new SVM-based algorithm for rank aggregation from pairwise data, and show that this converges to an optimal ranking under an even more general condition that we term `generalized low-noise'. In all cases, we provide explicit sample complexity bounds for exact recovery of an optimal ranking. Our experiments confirm our theoretical findings and help to shed light on the statistical behavior of various rank aggregation algorithms.

-

Jascha Sohl-Dickstein and Ben Poole and Surya Ganguli

Fast large-scale optimization by unifying stochastic gradient and quasi-Newton methods (pdf)

We present an algorithm for minimizing a sum of functions that combines the computational efficiency of stochastic gradient descent (SGD) with the second order curvature information leveraged by quasi-Newton methods. We unify these disparate approaches by maintaining an independent Hessian approximation for each contributing function in the sum. We maintain computational tractability and limit memory requirements even for high dimensional optimization problems by storing and manipulating these quadratic approximations in a shared, time evolving, low dimensional subspace. This algorithm contrasts with earlier stochastic second order techniques that treat the Hessian of each contributing function as a noisy approximation to the full Hessian, rather than as a target for direct estimation. Each update step requires only a single contributing function or minibatch evaluation (as in SGD), and each step is scaled using an approximate inverse Hessian and little to no adjustment of hyperparameters is required (as is typical for quasi-Newton methods). We experimentally demonstrate improved convergence on seven diverse optimization problems. The algorithm is released as open source Python and MATLAB packages.

-

Anoop Korattikara and Yutian Chen and Max Welling

Austerity in MCMC Land: Cutting the Metropolis-Hastings Budget (pdf)

Can we make Bayesian posterior MCMC sampling more efficient when faced with very large datasets? We argue that computing the likelihood for N datapoints in the Metropolis-Hastings (MH) test to reach a single binary decision is computationally inefficient. We introduce an approximate MH rule based on a sequential hypothesis test that allows us to accept or reject samples with high confidence using only a fraction of the data required for the exact MH rule. While this method introduces an asymptotic bias, we show that this bias can be controlled and is more than offset by a decrease in variance due to our ability to draw more samples per unit of time.

-

Mohamad Ali Torkamani and Daniel Lowd

On Robustness and Regularization of Structural Support Vector Machines (pdf)

Previous analysis of binary SVMs has demonstrated a deep connection between robustness to perturbations over uncertainty sets and regularization of the weights. In this paper, we explore the problem of learning robust models for structured prediction problems. We first formulate the problem of learning robust structural SVMs when there are perturbations in the feature space. We consider two different classes of uncertainty sets for the perturbations: ellipsoidal uncertainty sets and polyhedral uncertainty sets. In both cases, we show that the robust optimization problem is equivalent to the non-robust formulation with an additional regularizer. For the ellipsoidal uncertainty set, the additional regularizer is based on the dual norm of the norm that constrains the ellipsoidal uncertainty. For the polyhedral uncertainty set, we show that the robust optimization problem is equivalent to adding a linear regularizer in a transformed weight space related to the linear constraints of the polyhedron. We also show that these constraint sets can be combined and demonstrate a number of interesting special cases. This represents the first theoretical analysis of robust optimization of structural support vector machines. Our experimental results show that our method outperforms the nonrobust structural SVMs on real world data when the test data distributions is drifted from the training data distribution.

-

Raffay Hamid and Ying Xiao and Alex Gittens and Dennis Decoste

Compact Random Feature Maps (pdf)

Kernel approximation using randomized feature maps has recently gained a lot of interest. In this work, we identify that previous approaches for polynomial kernel approximation create maps that are rank deficient, and therefore do not utilize the capacity of the projected feature space effectively. To address this challenge, we propose compact random feature maps (CRAFTMaps) to approximate polynomial kernels more concisely and accurately. We prove the error bounds of CRAFTMaps demonstrating their superior kernel reconstruction performance compared to the previous approximation schemes. We show how structured random matrices can be used to efficiently generate CRAFTMaps, and present a single-pass algorithm using CRAFTMaps to learn non-linear multi-class classifiers. We present experiments on multiple standard data-sets with performance competitive with state-of-the-art results.

-

Joachim Giesen and Soeren Laue and Patrick Wieschollek

Robust and Efficient Kernel Hyperparameter Paths with Guarantees (pdf)

Algorithmically, many machine learning tasks boil down to solving parameterized optimization problems. Finding good values for the parameters has significant influence on the statistical performance of these methods. Thus supporting the choice of parameter values algorithmically has received quite some attention recently, especially algorithms for computing the whole solution path of parameterized optimization problem. These algorithms can be used, for instance, to track the solution of a regularized learning problem along the regularization parameter path, or for tracking the solution of kernelized problems along a kernel hyperparameter path. Since exact path following algorithms can be numerically unstable, robust and efficient approximate path tracking algorithms became popular for regularized learning problems. By now algorithms with optimal path complexity are known for many regularized learning problems. That is not the case for kernel hyperparameter path tracking algorithms, where the exact path tracking algorithms can also suffer from numerical instabilities. The robust approximation algorithms for regularization path tracking can not be used directly for kernel hyperparameter path tracking problems since the latter fall into a different problem class. Here we address this problem by devising a robust and efficient path tracking algorithm that can also handle kernel hyperparameter paths and has asymptotically optimal complexity. We use this algorithm to compute approximate kernel hyperparamter solution paths for support vector machines and robust kernel regression. Experimental results for this problem applied to various data sets confirms the theoretical complexity analysis.

-

Nikos Karampatziakis and Paul Mineiro

Discriminative Features via Generalized Eigenvectors (pdf)

Representing examples in a way that is compatible with the underlying classifier can greatly enhance the performance of a learning system. In this paper we investigate scalable techniques for inducing discriminative features by taking advantage of simple second order structure in the data. We focus on multiclass classification and show that features extracted from the generalized eigenvectors of the class conditional second moments lead to classifiers with excellent empirical performance. Moreover, these features have attractive theoretical properties, such as inducing representations that are invariant to linear transformations of the input. We evaluate classifiers built from these features on three different tasks, obtaining state of the art results.

-

Hsiang-Fu Yu and Prateek Jain and Purushottam Kar and Inderjit Dhillon

Large-scale Multi-label Learning with Missing Labels (pdf)

The multi-label classification problem has generated significant interest in recent years. However, existing approaches do not adequately address two key challenges: (a) scaling up to problems with a large number (say millions) of labels, and (b) handling data with missing labels. In this paper, we directly address both these problems by studying the multi-label problem in a generic empirical risk minimization (ERM) framework. Our framework, despite being simple, is surprisingly able to encompass several recent label-compression based methods which can be derived as special cases of our method. To optimize the ERM problem, we develop techniques that exploit the structure of specific loss functions - such as the squared loss function - to obtain efficient algorithms. We further show that our learning framework admits excess risk bounds even in the presence of missing labels. Our bounds are tight and demonstrate better generalization performance for low-rank promoting trace-norm regularization when compared to (rank insensitive) Frobenius norm regularization. Finally, we present extensive empirical results on a variety of benchmark datasets and show that our methods perform significantly better than existing label compression based methods and can scale up to very large datasets such as a Wikipedia dataset that has more than 200,000 labels.

-

Jun Liu and Zheng Zhao and Jie Wang and Jieping Ye

Safe Screening with Variational Inequalities and Its Application to Lasso (pdf)

Sparse learning techniques have been routinely used for feature selection as the resulting model usually has a small number of non-zero entries. Safe screening, which eliminates the features that are guaranteed to have zero coefficients for a certain value of the regularization parameter, is a technique for improving the computational efficiency. Safe screening is gaining increasing attention since 1) solving sparse learning formulations usually has a high computational cost especially when the number of features is large and 2) one needs to try several regularization parameters to select a suitable model. In this paper, we propose an approach called ``Sasvi" (Safe screening with variational inequalities). Sasvi makes use of the variational inequality that provides the sufficient and necessary optimality condition for the dual problem. Several existing approaches for Lasso screening can be casted as relaxed versions of the proposed Sasvi, thus Sasvi provides a stronger safe screening rule. We further study the monotone properties of Sasvi for Lasso, based on which a sure removal regularization parameter can be identified for each feature. Experimental results on both synthetic and real data sets are reported to demonstrate the effectiveness of the proposed Sasvi for Lasso screening.

-

Prateek Jain and Abhradeep Guha Thakurta

(Near) Dimension Independent Risk Bounds for Differentially Private Learning (pdf)

In this paper, we study the problem of differentially private risk minimization where the goal is to provide differentially private algorithms that have small excess risk. In particular we address the following open problem: \emph{Is it possible to design computationally efficient differentially private risk minimizers with excess risk bounds that do not explicitly depend on dimensionality ($p$) and do not require structural assumptions like restricted strong convexity?

-

Danilo Jimenez Rezende and Shakir Mohamed and Daan Wierstra

Stochastic Backpropagation and Approximate Inference in Deep Generative Models (pdf)

We marry ideas from deep neural networks and approximate Bayesian inference to derive a generalised class of deep, directed generative models, endowed with a new algorithm for scalable inference and learning. Our algorithm introduces a recognition model to represent an approximate posterior distribution and uses this for optimisation of a variational lower bound. We develop stochastic backpropagation -- rules for gradient backpropagation through stochastic variables -- and derive an algorithm that allows for joint optimisation of the parameters of both the generative and recognition models. We demonstrate on several real-world data sets that by using stochastic backpropagation and variational inference, we obtain models that are able to generate realistic samples of data, allow for accurate imputations of missing data, and provide a useful tool for high-dimensional data visualisation.

-

Yong Liu and Shali Jiang and Shizhong Liao

Efficient Approximation of Cross-Validation for Kernel Methods using Bouligand Influence Function (pdf)

Model selection is one of the key issues both in recent research and application of kernel methods. Cross-validation is a commonly employed and widely accepted model selection criterion. However, it requires multiple times of training the algorithm under consideration, which is computationally intensive. In this paper, we present a novel strategy for approximating the cross-validation based on the Bouligand influence function (BIF), which only requires the solution of the algorithm once. The BIF measures the impact of an infinitesimal small amount of contamination of the original distribution. We first establish the link between the concept of BIF and the concept of cross-validation. The BIF is related to the first order term of a Taylor expansion. Then, we calculate the BIF and higher order BIFs, and apply these theoretical results to approximate the cross-validation error in practice. Experimental results demonstrate that our approximate cross-validation criterion is sound and efficient.

-

Yuan Fang and Kevin Chang and Hady Lauw

Graph-based Semi-supervised Learning: Realizing Pointwise Smoothness Probabilistically (pdf)

As the central notion in semi-supervised learning, smoothness is often realized on a graph representation of the data. In this paper, we study two complementary dimensions of smoothness: its pointwise nature and probabilistic modeling. While no existing graph-based work exploits them in conjunction, we encompass both in a novel framework of Probabilistic Graph-based Pointwise Smoothness (PGP), building upon two foundational models of data closeness and label coupling. This new form of smoothness axiomatizes a set of probability constraints, which ultimately enables class prediction. Theoretically, we provide an error and robustness analysis of PGP. Empirically, we conduct extensive experiments to show the advantages of PGP.

-

David Inouye and Pradeep Ravikumar and Inderjit Dhillon

Admixture of Poisson MRFs: A Topic Model with Word Dependencies (pdf)

This paper introduces a new topic model based on an admixture of Poisson Markov Random Fields (APM), which can model dependencies between words as opposed to previous independent topic models such as PLSA (Hofmann, 1999), LDA (Blei et al., 2003) or SAM (Reisinger et al., 2010). We propose a class of admixture models that generalizes previous topic models and show an equivalence between the conditional distribution of LDA and independent Poissons—suggesting that APM subsumes the modeling power of LDA. We present a tractable method for estimating the parameters of an APM based on the pseudo log-likelihood and demonstrate the benefits of APM over previous models by preliminary qualitative and quantitative experiments.

-

Filipe Rodrigues and Francisco Pereira and Bernardete Ribeiro

Gaussian Process Classification and Active Learning with Multiple Annotators (pdf)

Learning from multiple annotators took a valuable step towards modelling data that does not fit the usual single annotator setting. However, multiple annotators sometimes offer varying degrees of expertise. When disagreements arise, the establishment of the correct label through trivial solutions such as majority voting may not be adequate, since without considering heterogeneity in the annotators, we risk generating a flawed model. In this paper, we extend GP classification in order to account for multiple annotators with different levels expertise. By explicitly handling uncertainty, Gaussian processes (GPs) provide a natural framework to build proper multiple-annotator models. We empirically show that our model significantly outperforms other commonly used approaches, such as majority voting, without a significant increase in the computational cost of approximate Bayesian inference. Furthermore, an active learning methodology is proposed, which is able to reduce annotation cost even further.

-

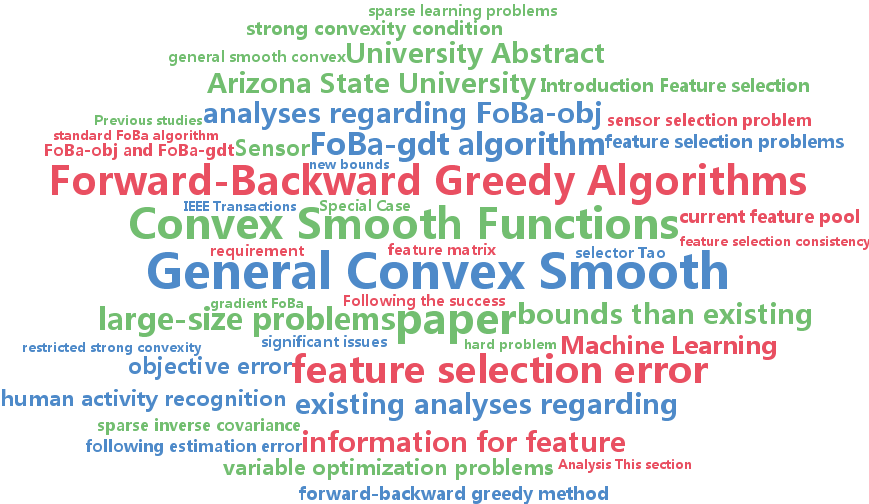

Ji Liu and Jieping Ye and Ryohei Fujimaki

Forward-Backward Greedy Algorithms for General Convex Smooth Functions over A Cardinality Constraint (pdf)

We consider forward-backward greedy algorithms for solving sparse feature selection problems with general convex smooth functions. A state-of-the-art greedy method, the Forward-Backward greedy algorithm (FoBa-obj) requires to solve a large number of optimization problems, thus it is not scalable for large-size problems. The FoBa-gdt algorithm, which uses the gradient information for feature selection at each forward iteration, significantly improves the efficiency of FoBa-obj. In this paper, we systematically analyze the theoretical properties of both algorithms. Our main contributions are: 1) We derive better theoretical bounds than existing analyses regarding FoBa-obj for general smooth convex functions; 2) We show that FoBa-gdt achieves the same theoretical performance as FoBa-obj under the same condition: restricted strong convexity condition. Our new bounds are consistent with the bounds of a special case (least squares) and fills a previously existing theoretical gap for general convex smooth functions; 3) We show that the restricted strong convexity condition is satisfied if the number of independent samples is more than $\bar{k

-

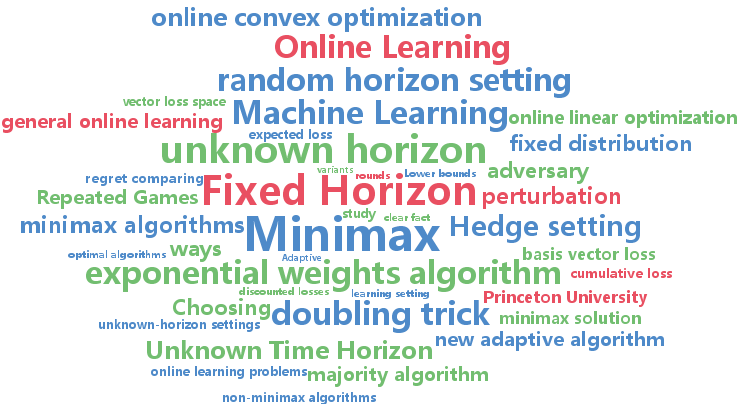

Haipeng Luo and Robert Schapire

Towards Minimax Online Learning with Unknown Time Horizon (pdf)

We consider online learning when the time horizon is unknown. We apply a minimax analysis, beginning with the fixed horizon case, and then moving on to two unknown-horizon settings, one that assumes the horizon is chosen randomly according to some distribution, and the other which allows the adversary full control over the horizon. For the random horizon setting with restricted losses, we derive a fully optimal minimax algorithm. And for the adversarial horizon setting, we prove a nontrivial lower bound which shows that the adversary obtains strictly more power than when the horizon is fixed and known. Based on the minimax solution of the random horizon setting, we then propose a new adaptive algorithm which ``pretends'' that the horizon is drawn from a distribution from a special family, but no matter how the actual horizon is chosen, the worst-case regret is of the optimal rate. Furthermore, our algorithm can be combined and applied in many ways, for instance, to online convex optimization, follow the perturbed leader, exponential weights algorithm and first order bounds. Experiments show that our algorithm outperforms many other existing algorithms in an online linear optimization setting.

-

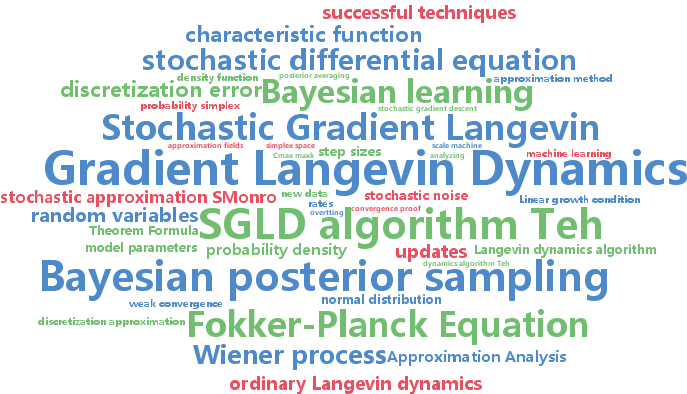

Issei Sato and Hiroshi Nakagawa

Approximation Analysis of Stochastic Gradient Langevin Dynamics by using Fokker-Planck Equation and Ito Process (pdf)

The stochastic gradient Langevin dynamics (SGLD) algorithm is appealing for large scale Bayesian learning. The SGLD algorithm seamlessly transit stochastic optimization and Bayesian posterior sampling. However, solid theories, such as convergence proof, have not been developed. We theoretically analyze the SGLD algorithm with constant stepsize in two ways. First, we show by using the Fokker-Planck equation that the probability distribution of random variables generated by the SGLD algorithm converges to the Bayesian posterior. Second, we analyze the convergence of the SGLD algorithm by using the Ito process, which reveals that the SGLD algorithm does not strongly but weakly converges. This result indicates that the SGLD algorithm can be an approximation method for posterior averaging.

-

Wenzhuo Yang and Melvyn Sim and Huan Xu

The Coherent Loss Function for Classification (pdf)

A prediction rule in binary classification that aims to achieve the lowest probability of misclassification involves minimizing over a non-convex, 0-1 loss function, which is typically a computationally intractable optimization problem. To address the intractability, previous methods consider minimizing the cumulative loss -- the sum of convex surrogates of the 0-1 loss of each sample. In this paper, we revisit this paradigm and develop instead an axiomatic framework by proposing a set of salient properties on functions for binary classification and then propose the coherent loss approach, which is a tractable upper-bound of the empirical classification error over the entire sample set. We show that the proposed approach yields a strictly tighter approximation to the empirical classification error than any convex cumulative loss approach while preserving the convexity of the underlying optimization problem, and this approach for binary classification also has a robustness interpretation which builds a connection to robust SVMs. The experimental results show that our approach outperforms the standard SVM when additional constraints are imposed.

-

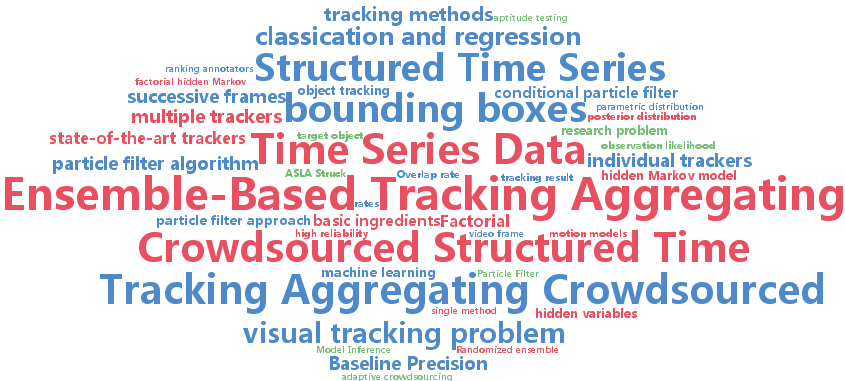

Naiyan Wang and Dit-Yan Yeung

Ensemble-Based Tracking: Aggregating Crowdsourced Structured Time Series Data (pdf)

We study the problem of aggregating the contributions of multiple contributors in a crowdsourcing setting. The data involved is in a form not typically considered in most crowdsourcing tasks, in that the data is structured and has a temporal dimension. In particular, we study the visual tracking problem in which the unknown data to be estimated is in the form of a sequence of bounding boxes representing the trajectory of the target object being tracked. We propose a factorial hidden Markov model (FHMM) for ensemble-based tracking by learning jointly the unknown trajectory of the target and the reliability of each tracker in the ensemble. For efficient online inference of the FHMM, we devise a conditional particle filter algorithm by exploiting the structure of the joint posterior distribution of the hidden variables. Using the largest open benchmark for visual tracking, we empirically compare two ensemble methods constructed from five state-of-the-art trackers with the individual trackers. The promising experimental results provide empirical evidence for our ensemble approach to "get the best of all worlds".

-

Krikamol Muandet and Kenji Fukumizu and Bharath Sriperumbudur and Arthur Gretton and Bernhard Schoelkopf

Kernel Mean Estimation and Stein Effect (pdf)

A mean function in reproducing kernel Hilbert space (RKHS), or a kernel mean, is an important part of many algorithms ranging from kernel principal component analysis to Hilbert-space embedding of distributions. Given a finite sample, an empirical average is the standard estimate for the true kernel mean. We show that this estimator can be improved due to a well-known phenomenon in statistics called Stein phenomenon. After consideration, our theoretical analysis reveals the existence of a wide class of estimators that are better than the standard one. Focusing on a subset of this class, we propose efficient shrinkage estimators for the kernel mean. Empirical evaluations on several applications clearly demonstrate that the proposed estimators outperform the standard kernel mean estimator.

-

Francesco Orabona and Tamir Hazan and Anand Sarwate and Tommi Jaakkola

On Measure Concentration of Random Maximum A-Posteriori Perturbations (pdf)

The maximum a-posteriori (MAP) perturbation framework has emerged as a useful approach for inference and learning in high dimensional complex models. By maximizing a randomly perturbed potential function, MAP perturbations generate unbiased samples from the Gibbs distribution. Unfortunately, the computational cost of generating so many high-dimensional random variables can be prohibitive. More efficient algorithms use sequential sampling strategies based on the expected value of low dimensional MAP perturbations. This paper develops new measure concentration inequalities that bound the number of samples needed to estimate such expected values. Applying the general result to MAP perturbations can yield a more efficient algorithm to approximate sampling from the Gibbs distribution. The measure concentration result is of general interest and may be applicable to other areas involving Monte Carlo estimation of expectations.

-

Alessio Benavoli and Giorgio Corani and Francesca Mangili and Marco Zaffalon and Fabrizio Ruggeri

A Bayesian Wilcoxon signed-rank test based on the Dirichlet process (pdf)

Bayesian methods are ubiquitous in machine learning. Nevertheless, the analysis of empirical results is typically performed by frequentist tests. This implies dealing with null hypothesis significance tests and p-values, even though the shortcomings of such methods are well known. We propose a nonparametric Bayesian version of the Wilcoxon signed-rank test using a Dirichlet process (DP) based prior. We address in two different ways the problem of how to choose the infinite dimensional parameter that characterizes the DP. The proposed test has all the traditional strengths of the Bayesian approach; for instance, unlike the frequentist tests, it allows verifying the null hypothesis, not only rejecting it, and taking decision which minimize the expected loss. Moreover, one of the solutions proposed to model the infinitedimensional parameter of the DP, allows isolating instances in which the traditional frequentist test is guessing at random. We show results dealing with the comparison of two classifiers using real and simulated data.

-

Souhaib Ben Taieb and Rob Hyndman

Boosting multi-step autoregressive forecasts (pdf)

Multi-step forecasts can be produced recursively by iterating a one-step model, or directly using a specific model for each horizon. Choosing between these two strategies is not an easy task since it involves a trade-off between bias and estimation variance over the forecast horizon. Using a nonlinear machine learning model makes the tradeoff even more difficult. To address this issue, we propose a new forecasting strategy which boosts traditional recursive linear forecasts with a direct strategy using a boosting autoregression procedure at each horizon. First, we investigate the performance of the proposed strategy in terms of bias and variance decomposition of the error using simulated time series. Then, we evaluate the proposed strategy on real-world time series from two forecasting competitions. Overall, we obtain excellent performance with respect to the standard forecasting strategies.

-

Michal Valko and Remi Munos and Branislav Kveton and Tomáš Kocák

Spectral Bandits for Smooth Graph Functions (pdf)

Smooth functions on graphs have wide applications in manifold and semi-supervised learning. In this paper, we study a bandit problem where the payoffs of arms are smooth on a graph. This framework is suitable for solving online learning problems that involve graphs, such as content-based recommendation. In this problem, each item we can recommend is a node and its expected rating is similar to its neighbors. The goal is to recommend items that have high expected ratings. We aim for the algorithms where the cumulative regret with respect to the optimal policy would not scale poorly with the number of nodes. In particular, we introduce the notion of an effective dimension, which is small in real-world graphs, and propose two algorithms for solving our problem that scale linearly and sublinearly in this dimension. Our experiments on real-world content recommendation problem show that a good estimator of user preferences for thousands of items can be learned from just tens of nodes evaluations.

-

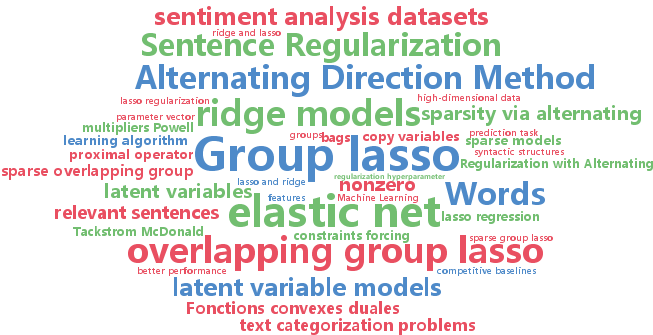

Dani Yogatama and Noah Smith

Making the Most of Bag of Words: Sentence Regularization with Alternating Direction Method of Multipliers (pdf)

In many high-dimensional learning problems, only some parts of an observation are important to the prediction task; for example, the cues to correctly categorizing a document may lie in a handful of its sentences. We introduce a learning algorithm that exploits this intuition by encoding it in a regularizer. Specifically, we apply the sparse overlapping group lasso with one group for every bundle of features occurring together in a training-data sentence, leading to thousands to millions of overlapping groups. We show how to efficiently solve the resulting optimization challenge using the alternating directions method of multipliers. We find that the resulting method significantly outperforms competitive baselines (standard ridge, lasso, and elastic net regularizers) on a suite of real-world text categorization problems.

-

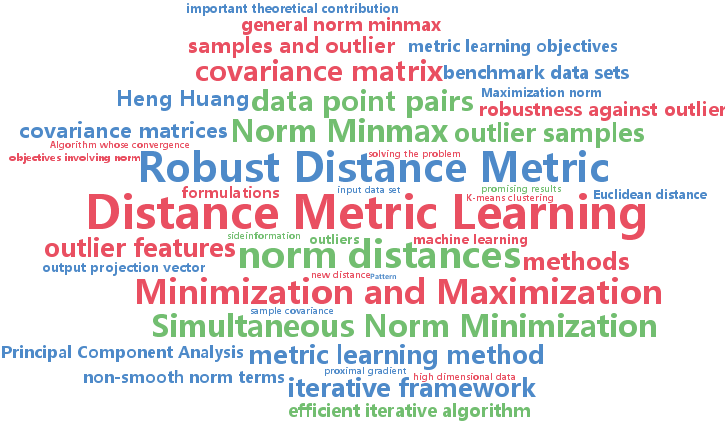

Hua Wang and Feiping Nie and Heng Huang

Robust Distance Metric Learning via Simultaneous L1-Norm Minimization and Maximization (pdf)

Traditional distance metric learning with side information usually formulates the objectives using the covariance matrices of the data point pairs in the two constraint sets of must-links and cannot-links. Because the covariance matrix computes the sum of the squared L2-norm distances, it is prone to both outlier samples and outlier features. To develop a robust distance metric learning method, in this paper we propose a new objective for distance metric learning using the L1-norm distances. However, the resulted objective is very challenging to solve, because it simultaneously minimizes and maximizes (minmax) a number of non-smooth L1-norm terms. As an important theoretical contribution of this paper, we systematically derive an efficient iterative algorithm to solve the general L1-norm minmax problem, which is rarely studied in literature. We have performed extensive empirical evaluations, where our new distance metric learning method outperforms related state-of-the-art methods in a variety of experimental settings to cluster both noiseless and noisy data.

-

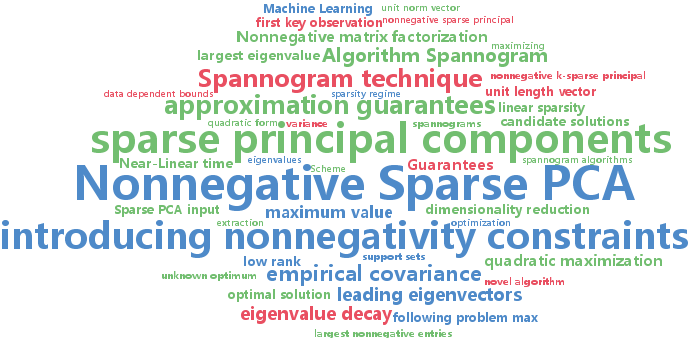

Megasthenis Asteris and Dimitris Papailiopoulos and Alexandros Dimakis

Nonnegative Sparse PCA with Provable Guarantees (pdf)

We introduce a novel algorithm to compute nonnegative sparse principal components of positive semidefinite (PSD) matrices. Our algorithm comes with approximation guarantees contingent on the spectral profile of the input matrix A: the sharper the eigenvalue decay, the better the approximation quality. If the eigenvalues decay like any asymptotically vanishing function, we can approximate nonnegative sparse PCA within any accuracy $\epsilon$ in time polynomial in the matrix size $n$ and desired sparsity k, but not in $1/\epsilon$. Further, we obtain a data-dependent bound that is computed by executing an algorithm on a given data set. This bound is significantly tighter than a-priori bounds and can be used to show that for all tested datasets our algorithm is provably within 40%-90% from the unknown optimum. Our algorithm is combinatorial and explores a subspace defined by the leading eigenvectors of A. We test our scheme on several data sets, showing that it matches or outperforms the previous state of the art.

-

Sebastien Bratieres and Novi Quadrianto and Sebastian Nowozin and Zoubin Ghahramani

Scalable Gaussian Process Structured Prediction for Grid Factor Graph Applications (pdf)

Structured prediction is an important and well studied problem with many applications across machine learning. GPstruct is a recently proposed structured prediction model that offers appealing properties such as being kernelised, non-parametric, and supporting Bayesian inference (Bratières et al. 2013). The model places a Gaussian process prior over energy functions which describe relationships between input variables and structured output variables. However, the memory demand of GPstruct is quadratic in the number of latent variables and training runtime scales cubically. This prevents GPstruct from being applied to problems involving grid factor graphs, which are prevalent in computer vision and spatial statistics applications. Here we explore a scalable approach to learning GPstruct models based on ensemble learning, with weak learners (predictors) trained on subsets of the latent variables and bootstrap data, which can easily be distributed. We show experiments with 4M latent variables on image segmentation. Our method outperforms widely-used conditional random field models trained with pseudo-likelihood. Moreover, in image segmentation problems it improves over recent state-of-the-art marginal optimisation methods in terms of predictive performance and uncertainty calibration. Finally, it generalises well on all training set sizes.

-

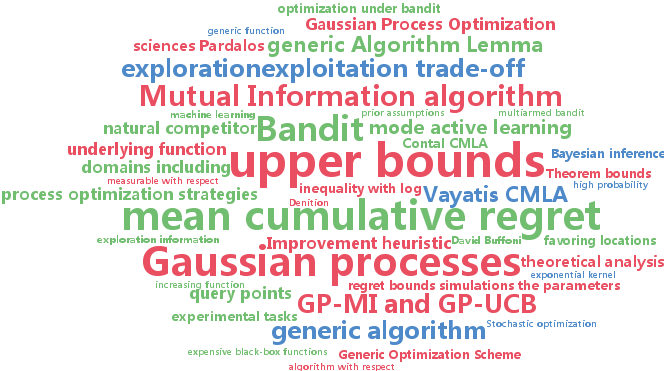

Emile Contal and Vianney Perchet and Nicolas Vayatis

Gaussian Process Optimization with Mutual Information (pdf)

In this paper, we analyze a generic algorithm scheme for sequential global optimization using Gaussian processes. The upper bounds we derive on the cumulative regret for this generic algorithm improve by an exponential factor the previously known bounds for algorithms like GP-UCB. We also introduce the novel Gaussian Process Mutual Information algorithm (GP-MI), which significantly improves further these upper bounds for the cumulative regret. We confirm the efficiency of this algorithm on synthetic and real tasks against the natural competitor, GP-UCB, and also the Expected Improvement heuristic.

-

Shashank Singh and Barnabas Poczos

Generalized Exponential Concentration Inequality for Renyi Divergence Estimation (pdf)

Estimating divergences between probability distributions in a consistent way is of great importance in many machine learning tasks. Although this is a fundamental problem in nonparametric statistics, to the best of our knowledge there has been no finite sample exponential inequality convergence bound derived for any divergence estimators. The main contribution of our work is to provide such a bound for an estimator of Renyi divergence for a smooth Holder class of densities on the d-dimensional unit cube. We also illustrate our theoretical results with a numerical experiment.

-

Jacob Steinhardt and Percy Liang

Adaptivity and Optimism: An Improved Exponentiated Gradient Algorithm (pdf)

We present an adaptive variant of the exponentiated gradient algorithm. Leveraging the optimistic learning framework of Rakhlin & Sridharan (2012), we obtain regret bounds that in the learning from experts setting depend on the variance and path length of the best expert, improving on results by Hazan & Kale (2008) and Chiang et al. (2012), and resolving an open problem posed by Kale (2012). Our techniques naturally extend to matrix-valued loss functions, where we present an adaptive matrix exponentiated gradient algorithm. To obtain the optimal regret bound in the matrix case, we generalize the Follow-the-Regularized-Leader algorithm to vector-valued payoffs, which may be of independent interest.

-

Tianqi Chen and Emily Fox and Carlos Guestrin

Stochastic Gradient Hamiltonian Monte Carlo (pdf)

Hamiltonian Monte Carlo (HMC) sampling methods provide a mechanism for defining distant proposals with high acceptance probabilities in a Metropolis-Hastings framework, enabling more efficient exploration of the state space than standard random-walk proposals. The popularity of such methods has grown significantly in recent years. However, a limitation of HMC methods is the required gradient computation for simulation of the Hamiltonian dynamical system-such computation is infeasible in problems involving a large sample size or streaming data. Instead, we must rely on a noisy gradient estimate computed from a subset of the data. In this paper, we explore the properties of such a stochastic gradient HMC approach. Surprisingly, the natural implementation of the stochastic approximation can be arbitrarily bad. To address this problem we introduce a variant that uses second-order Langevin dynamics with a friction term that counteracts the effects of the noisy gradient, maintaining the desired target distribution as the invariant distribution. Results on simulated data validate our theory. We also provide an application of our methods to a classification task using neural networks and to online Bayesian matrix factorization.

-

Taco Cohen and Max Welling

Learning the Irreducible Representations of Commutative Lie Groups (pdf)

We present a new probabilistic model of compact commutative Lie groups that produces invariant-equivariant and disentangled representations of data. To define the notion of disentangling, we borrow a fundamental principle from physics that is used to derive the elementary particles of a system from its symmetries. Our model employs a newfound Bayesian conjugacy relation that enables fully tractable probabilistic inference over compact commutative Lie groups -- a class that includes the groups that describe the rotation and cyclic translation of images. We train the model on pairs of transformed image patches, and show that the learned invariant representation is highly effective for classification.

-

Amirmohammad Rooshenas and Daniel Lowd

Learning Sum-Product Networks with Direct and Indirect Variable Interactions (pdf)

Sum-product networks (SPNs) are a deep probabilistic representation that allows for efficient, exact inference. SPNs generalize many other tractable models, including thin junction trees, latent tree models, and many types of mixtures. Previous work on learning SPN structure has mainly focused on using top-down or bottom-up clustering to find mixtures, which capture variable interactions indirectly through implicit latent variables. In contrast, most work on learning graphical models, thin junction trees, and arithmetic circuits has focused on finding direct interactions among variables. In this paper, we present ID-SPN, a new algorithm for learning SPN structure that unifies the two approaches. In experiments on 20 benchmark datasets, we find that the combination of direct and indirect interactions leads to significantly better accuracy than several state-of-the-art algorithms for learning SPNs and other tractable models.

-

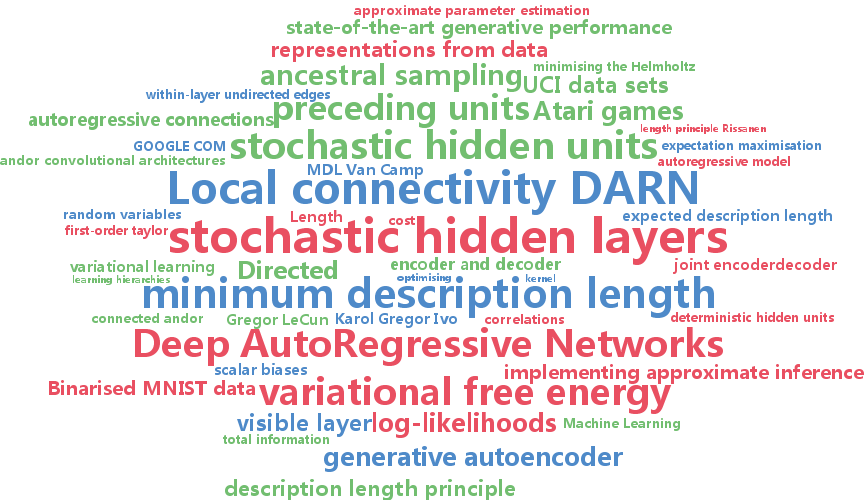

Karol Gregor and Ivo Danihelka and Andriy Mnih and Charles Blundell and Daan Wierstra

Deep AutoRegressive Networks (pdf)

We introduce a deep, generative autoencoder capable of learning hierarchies of distributed representations from data. Successive deep stochastic hidden layers are equipped with autoregressive connections, which enable the model to be sampled from quickly and exactly via ancestral sampling. We derive an efficient approximate parameter estimation method based on the minimum description length (MDL) principle, which can be seen as maximising a variational lower bound on the log-likelihood, with a feedforward neural network implementing approximate inference. We demonstrate state-of-the-art generative performance on a number of classic data sets: several UCI data sets, MNIST and Atari 2600 games.

-

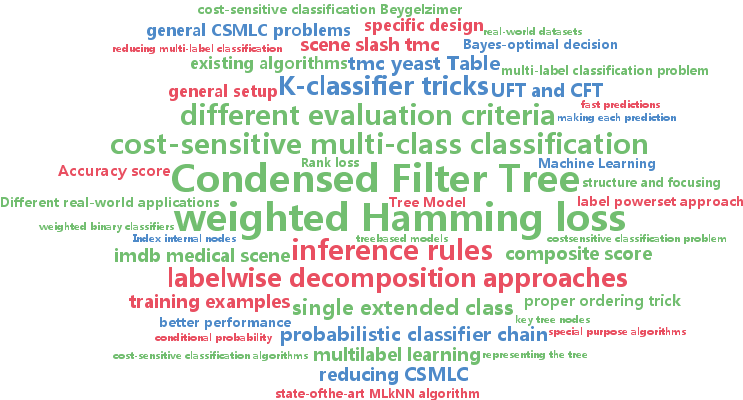

Chun-Liang Li and Hsuan-Tien Lin

Condensed Filter Tree for Cost-Sensitive Multi-Label Classification (pdf)

Different real-world applications of multi-label classification often demand different evaluation criteria. We formalize this demand with a general setup, cost-sensitive multi-label classification (CSMLC), which takes the evaluation criteria into account during learning. Nevertheless, most existing algorithms can only focus on optimizing a few specific evaluation criteria, and cannot systematically deal with different ones. In this paper, we propose a novel algorithm, called condensed filter tree (CFT), for optimizing any criteria in CSMLC. CFT is derived from reducing CSMLC to the famous filter tree algorithm for cost-sensitive multi-class classification via constructing the label powerset. We successfully cope with the difficulty of having exponentially many extended-classes within the powerset for representation, training and prediction by carefully designing the tree structure and focusing on the key nodes. Experimental results across many real-world datasets validate that CFT is competitive with special purpose algorithms on special criteria and reaches better performance on general criteria.

-

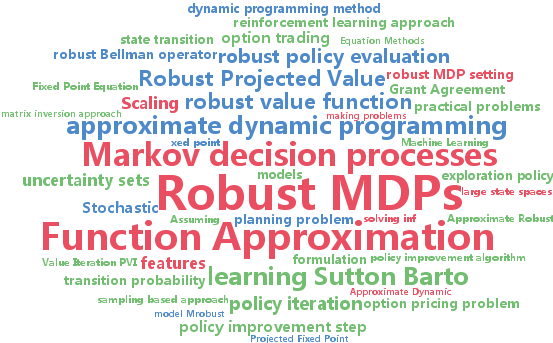

Aviv Tamar and Shie Mannor and Huan Xu

Scaling Up Robust MDPs using Function Approximation (pdf)

We consider large-scale Markov decision processes (MDPs) with parameter uncertainty, under the robust MDP paradigm. Previous studies showed that robust MDPs, based on a minimax approach to handling uncertainty, can be solved using dynamic programming for small to medium sized problems. However, due to the "curse of dimensionality", MDPs that model real-life problems are typically prohibitively large for such approaches. In this work we employ a reinforcement learning approach to tackle this planning problem: we develop a robust approximate dynamic programming method based on a projected fixed point equation to approximately solve large scale robust MDPs. We show that the proposed method provably succeeds under certain technical conditions, and demonstrate its effectiveness through simulation of an option pricing problem. To the best of our knowledge, this is the first attempt to scale up the robust MDP paradigm.

-

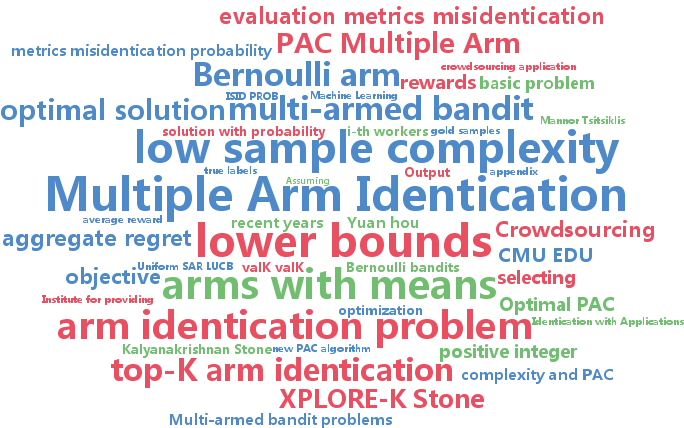

Yuan Zhou and Xi Chen and Jian Li

Optimal PAC Multiple Arm Identification with Applications to Crowdsourcing (pdf)

We study the problem of selecting $K$ arms with the highest expected rewards in a stochastic $N$-armed bandit game. Instead of using existing evaluation metrics (e.g., misidentification probability or the metric in EXPLORE-K), we propose to use the aggregate regret, which is defined as the gap between the average reward of the optimal solution and that of our solution. Besides being a natural metric by itself, we argue that in many applications, such as our motivating example from crowdsourcing, the aggregate regret bound is more suitable. We propose a new PAC algorithm, which, with probability at least $1-\delta$, identifies a set of $K$ arms with regret at most $\epsilon$. We provide the sample complexity bound of our algorithm. To complement, we establish the lower bound and show that the sample complexity of our algorithm matches the lower bound. Finally, we report experimental results on both synthetic and real data sets, which demonstrates the superior performance of the proposed algorithm.

-

Daryl Lim and Gert Lanckriet

Efficient Learning of Mahalanobis Metrics for Ranking (pdf)

We develop an efficient algorithm to learn a Mahalanobis distance metric by directly optimizing a ranking loss. Our approach focuses on optimizing the top of the induced rankings, which is desirable in tasks such as visualization and nearest-neighbor retrieval. We further develop and justify a simple technique to reduce training time significantly with minimal impact on performance. Our proposed method significantly outperforms alternative methods on several real-world tasks, and can scale to large and high-dimensional data.

-

Benigno Uria and Iain Murray and Hugo Larochelle

A Deep and Tractable Density Estimator (pdf)

The Neural Autoregressive Distribution Estimator (NADE) and its real-valued version RNADE are competitive density models of multidimensional data across a variety of domains. These models use a fixed, arbitrary ordering of the data dimensions. One can easily condition on variables at the beginning of the ordering, and marginalize out variables at the end of the ordering, however other inference tasks require approximate inference. In this work we introduce an efficient procedure to simultaneously train a NADE model for each possible ordering of the variables, by sharing parameters across all these models. We can thus use the most convenient model for each inference task at hand, and ensembles of such models with different orderings are immediately available. Moreover, unlike the original NADE, our training procedure scales to deep models. Empirically, ensembles of Deep NADE models obtain state of the art density estimation performance.

-

Samaneh Azadi and Suvrit Sra

Towards an optimal stochastic alternating direction method of multipliers (pdf)

We study regularized stochastic convex optimization subject to linear equality constraints. This class of problems was recently also studied by Ouyang et al. (2013) and Suzuki (2013); both introduced similar stochastic alternating direction method of multipliers (SADMM) algorithms. However, the analysis of both papers led to suboptimal convergence rates. This paper presents two new SADMM methods: (i) the first attains the minimax optimal rate of O(1/k) for nonsmooth strongly-convex stochastic problems; while (ii) the second progresses towards an optimal rate by exhibiting an O(1/k^2) rate for the smooth part. We present several experiments with our new methods; the results indicate improved performance over competing ADMM methods.

-

CORINNA CORTES and Mehryar Mohri and Umar Syed

Deep Boosting (pdf)

We present a new ensemble learning algorithm, DeepBoost, which can use as base classifiers a hypothesis set containing deep decision trees, or members of other rich or complex families, and succeed in achieving high accuracy without overfitting the data. The key to the success of the algorithm is a 'capacity-conscious' criterion for the selection of the hypotheses. We give new data-dependent learning bounds for convex ensembles expressed in terms of the Rademacher complexities of the sub-families composing the base classifier set, and the mixture weight assigned to each sub-family. Our algorithm directly benefits from these guarantees since it seeks to minimize the corresponding learning bound. We give a full description of our algorithm, including the details of its derivation, and report the results of several experiments showing that its performance compares favorably to that of AdaBoost and Logistic Regression and their L_1-regularized variants.

-

CORINNA CORTES and Vitaly Kuznetsov and Mehryar Mohri

Ensemble Methods for Structured Prediction (pdf)

We present a series of learning algorithms and theoretical guarantees for designing accurate ensembles of structured prediction tasks. This includes several randomized and deterministic algorithms devised by converting on-line learning algorithms to batch ones, and a boosting-style algorithm applicable in the context of structured prediction with a large number of labels. We give a detailed study of all these algorithms, including the description of new on-line-to-batch conversions and learning guarantees. We also report the results of extensive experiments with these algorithms in several structured prediction tasks.

-

Misha Denil and David Matheson and Nando De Freitas

Narrowing the Gap: Random Forests In Theory and In Practice (pdf)

Despite widespread interest and practical use, the theoretical properties of random forests are still not well understood. In this paper we contribute to this understanding in two ways. We present a new theoreti- cally tractable variant of random regression forests and prove that our algorithm is con- sistent. We also provide an empirical eval- uation, comparing our algorithm and other theoretically tractable random forest models to the random forest algorithm used in prac- tice. Our experiments provide insight into the relative importance of different simplifi- cations that theoreticians have made to ob- tain tractable models for analysis.

-

Jun-Kun Wang and Shou-de Lin

Robust Inverse Covariance Estimation under Noisy Measurements (pdf)

This paper proposes a robust method to estimate the inverse covariance under noisy measurements. The method is based on the estimation of each column in the inverse covariance matrix independently via robust regression, which enables parallelization. Different from previous linear programming based methods that cannot guarantee a positive semi-definite covariance matrix, our method adjusts the learned matrix to satisfy this condition, which further facilitates the tasks of forecasting future values. Experiments on time series prediction and classification under noisy condition demonstrate the effectiveness of the approach.

-

Peng Sun and Tong Zhang and Jie Zhou

A Convergence Rate Analysis for LogitBoost, MART and Their Variant (pdf)

LogitBoost, MART and their variant can be viewed as additive tree regression using logistic loss and boosting style optimization. We analyze their convergence rates based on a new weak learnability formulation. We show that it has $O(\frac{1

-

Shang-Tse Chen and Hsuan-Tien Lin and Chi-Jen Lu

Boosting with Online Binary Learners for the Multiclass Bandit Problem (pdf)

We consider the problem of online multiclass prediction in the bandit setting. Compared with the full-information setting, in which the learner can receive the true label as feedback after making each prediction, the bandit setting assumes that the learner can only know the correctness of the predicted label. Because the bandit setting is more restricted, it is difficult to design good bandit learners and currently there are not many bandit learners. In this paper, we propose an approach that systematically converts existing online binary classifiers to promising bandit learners with strong theoretical guarantee. The approach matches the idea of boosting, which has been shown to be powerful for batch learning as well as online learning. In particular, we establish the weak-learning condition on the online binary classifiers, and show that the condition allows automatically constructing a bandit learner with arbitrary strength by combining several of those classifiers. Experimental results on several real-world data sets demonstrate the effectiveness of the proposed approach.

-

Alexandre Lacoste and Mario Marchand and Fran�ois Laviolette and Hugo Larochelle

Agnostic Bayesian Learning of Ensembles (pdf)

We propose a method for producing ensembles of predictors based on holdout estimations of their generalization performances. This approach uses a prior directly on the performance of predictors taken from a finite set of candidates and attempts to infer which one is best. Using Bayesian inference, we can thus obtain a posterior that represents our uncertainty about that choice and construct a weighted ensemble of predictors accordingly. This approach has the advantage of not requiring that the predictors be probabilistic themselves, can deal with arbitrary measures of performance and does not assume that the data was actually generated from any of the predictors in the ensemble. Since the problem of finding the best (as opposed to the true) predictor among a class is known as agnostic PAC-learning, we refer to our method as agnostic Bayesian learning. We also propose a method to address the case where the performance estimate is obtained from k-fold cross validation. While being efficient and easily adjustable to any loss function, our experiments confirm that the agnostic Bayes approach is state of the art compared to common baselines such as model selection based on k-fold cross-validation or a linear combination of predictor outputs.

-

Si Si and Cho-Jui Hsieh and Inderjit Dhillon

Memory Efficient Kernel Approximation (pdf)

The scalability of kernel machines is a big challenge when facing millions of samples due to storage and computation issues for large kernel matrices, that are usually dense. Recently, many papers have suggested tackling this problem by using a low rank approximation of the kernel matrix. In this paper, we first make the observation that the structure of shift-invariant kernels changes from low-rank to block-diagonal (without any low-rank structure) when varying the scale parameter. Based on this observation, we propose a new kernel approximation algorithm -- Memory Efficient Kernel Approximation (MEKA), which considers both low-rank and clustering structure of the kernel matrix. We show that the resulting algorithm outperforms state-of-the-art low-rank kernel approximation methods in terms of speed, approximation error, and memory usage. As an example, on the MNIST2M dataset with two-million samples, our method takes 550 seconds on a single machine using less than 500 MBytes memory to achieve 0.2313 test RMSE for kernel ridge regression, while standard Nystr\{o

-

David Silver and Guy Lever and Nicolas Heess and Thomas Degris and Daan Wierstra and Martin Riedmiller

Deterministic Policy Gradient Algorithms (pdf)

In this paper we consider deterministic policy gradient algorithms for reinforcement learning with continuous actions. The deterministic policy gradient has a particularly appealing form: it is the expected gradient of the action-value function. This simple form means that the deterministic policy gradient can be estimated much more efficiently than the usual stochastic policy gradient. To ensure adequate exploration, we introduce an off-policy actor-critic algorithm that learns a deterministic target policy from an exploratory behaviour policy. Deterministic policy gradient algorithms outperformed their stochastic counterparts in several benchmark problems, particularly in high-dimensional action spaces.

-

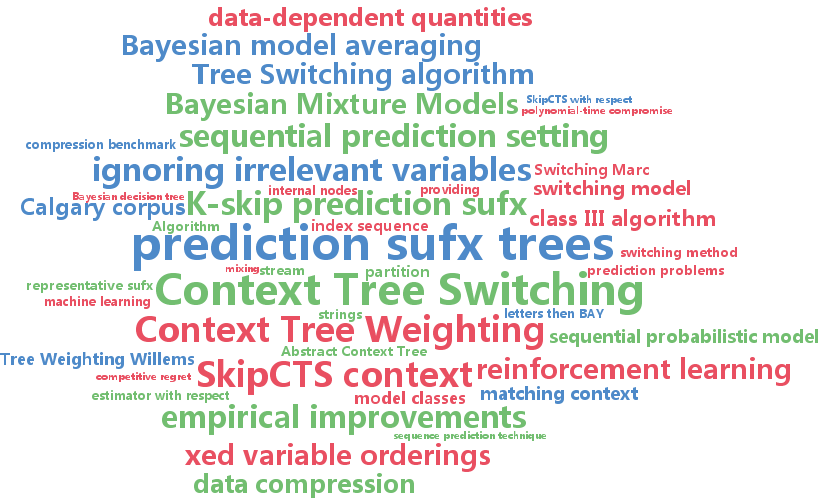

Marc Bellemare and Joel Veness and Erik Talvitie

Skip Context Tree Switching (pdf)

Context Tree Weighting (CTW) is a powerful probabilistic sequence prediction technique that efficiently performs Bayesian model averaging over the class of all prediction suffix trees of bounded depth. In this paper we show how to generalize this technique to the class of K-skip prediction suffix trees. Contrary to regular prediction suffix trees, K-skip prediction suffix trees are permitted to ignore up to K contiguous portions of the context. This allows for significant improvements in predictive accuracy when irrelevant variables are present, a case which often occurs within record-aligned data and images. We provide a regret-based analysis of our approach, and empirically evaluate it on the Calgary corpus and a set of Atari 2600 screen prediction tasks.

-

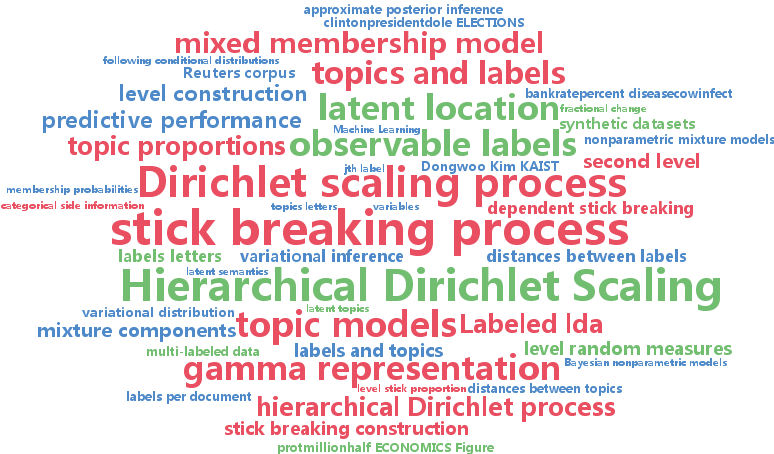

Dongwoo Kim and Alice Oh

Hierarchical Dirichlet Scaling Process (pdf)

We present the hierarchical Dirichlet scaling process (HDSP), a Bayesian nonparametric mixed membership model for multi-labeled data. We construct the HDSP based on the gamma representation of the hierarchical Dirichlet process (HDP) which allows scaling the mixture components. With such construction, HDSP allocates a latent location to each label and mixture component in a space, and uses the distance between them to guide membership probabilities. We develop a variational Bayes algorithm for the approximate posterior inference of the HDSP. Through experiments on synthetic datasets as well as datasets of newswire, medical journal articles, and Wikipedia, we show that the HDSP results in better predictive performance than HDP, labeled LDA and partially labeled LDA.

-

Mohammad Gheshlaghi azar and Alessandro Lazaric and Emma Brunskill

Online Stochastic Optimization under Correlated Bandit Feedback (pdf)

In this paper we consider the problem of online stochastic optimization of a locally smooth function under bandit feedback. We introduce the high-confidence tree (HCT) algorithm, a novel anytime $\mathcal X$-armed bandit algorithm, and derive regret bounds matching the performance of state-of-the-art algorithms in terms of the dependency on number of steps and the near-optimality dimension. The main advantage of HCT is that it handles the challenging case of correlated bandit feedback (reward), whereas existing methods require rewards to be conditionally independent. HCT also improves on the state-of-the-art in terms of the memory requirement, as well as requiring a weaker smoothness assumption on the mean-reward function in comparison with the existing anytime algorithms. Finally, we discuss how HCT can be applied to the problem of policy search in reinforcement learning and we report preliminary empirical results.

-

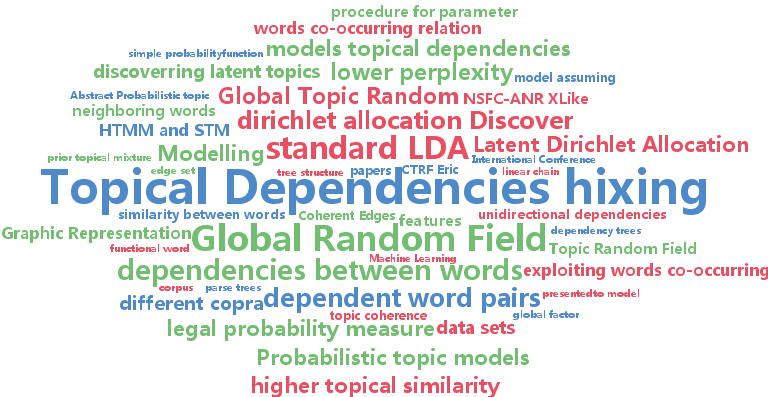

Zhixing Li and Siqiang Wen and Juanzi Li and Peng Zhang and Jie Tang

On Modelling Non-linear Topical Dependencies (pdf)

Probabilistic topic models such as Latent Dirichlet Allocation (LDA) discover latent topics from large corpora by exploiting words' co-occurring relation. By observing the topical similarity between words, we find that some other relations, such as semantic or syntax relation between words, lead to strong dependence between their topics. In this paper, sentences are represented as dependency trees and a Global Topic Random Field (GTRF) is presented to model the non-linear dependencies between words. To infer our model, a new global factor is defined over all edges and the normalization factor of GRF is proven to be a constant. As a result, no independent assumption is needed when inferring our model. Based on it, we develop an efficient expectation-maximization (EM) procedure for parameter estimation. Experimental results on four data sets show that GTRF achieves much lower perplexity than LDA and linear dependency topic models and produces better topic coherence.

-

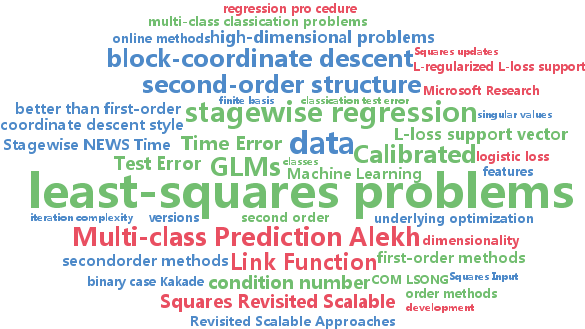

Alekh Agarwal and Sham Kakade and Nikos Karampatziakis and Le Song and Gregory Valiant

Least Squares Revisited: Scalable Approaches for Multi-class Prediction (pdf)

This work provides simple algorithms for multi-class (and multi-label) prediction in settings where both the number of examples $n$ and the data dimension $d$ are relatively large. These robust and parameter free algorithms are essentially iterative least-squares updates and very versatile both in theory and in practice. On the theoretical front, we present several variants with convergence guarantees. Owing to their effective use of second-order structure, these algorithms are substantially better than first-order methods in many practical scenarios. On the empirical side, we show how to scale our approach to high dimensional datasets, achieving dramatic computational speedups over popular optimization packages such as Liblinear and Vowpal Wabbit on standard datasets (MNIST and CIFAR-10), while attaining state-of-the-art accuracies.

-

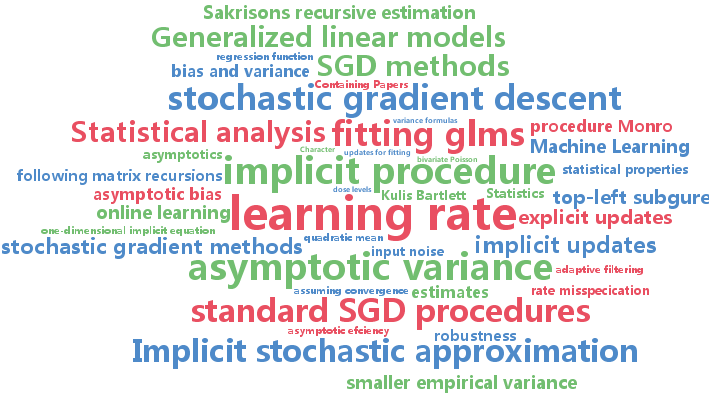

Panagiotis Toulis and Edoardo Airoldi and Jason Rennie

Statistical analysis of stochastic gradient methods for generalized linear models (pdf)

We study the statistical properties of stochastic gradient descent (SGD) using explicit and implicit updates for fitting generalized linear models (GLMs). Initially, we develop a computationally efficient algorithm to implement implicit SGD learning of GLMs. Next, we obtain exact formulas for the bias and variance of both updates which leads to two important observations on their comparative statistical properties. First, in small samples, the estimates from the implicit procedure are more biased than the estimates from the explicit one, but their empirical variance is smaller and they are more robust to learning rate misspecification. Second, the two procedures are statistically identical in the limit: they are both unbiased, converge at the same rate and have the same asymptotic variance. Our set of experiments confirm our theory and more broadly suggest that the implicit procedure can be a competitive choice for fitting large-scale models, especially when robustness is a concern.

-

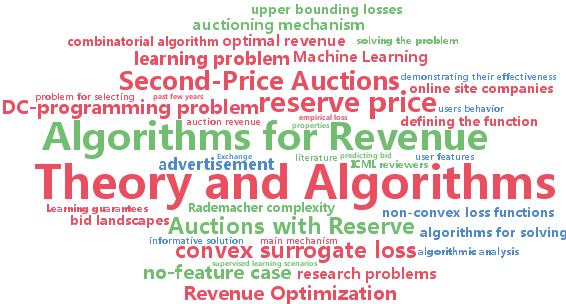

Andres Munoz Medina and Mehryar Mohri

Learning Theory and Algorithms for revenue optimization in second price auctions with reserve (pdf)

Second-price auctions with reserve play a critical role for modern search engine and popular online sites since the revenue of these companies often directly depends on the outcome of such auctions. The choice of the reserve price is the main mechanism through which the auction revenue can be influenced in these electronic markets. We cast the problem of selecting the reserve price to optimize revenue as a learning problem and present a full theoretical analysis dealing with the complex properties of the corresponding loss function (it is non-convex and discontinuous). We further give novel algorithms for solving this problem and report the results of encouraging experiments demonstrating their effectiveness.

-

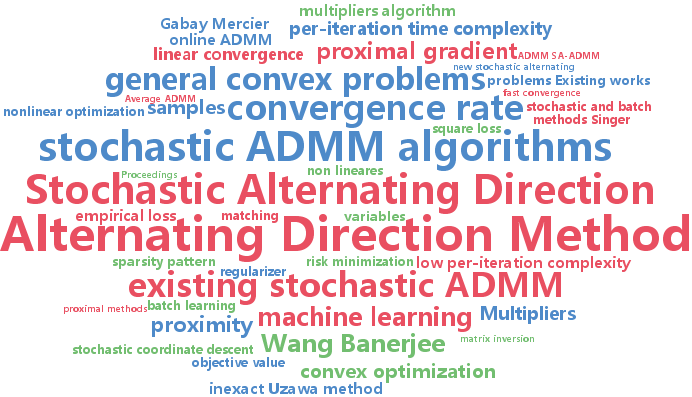

Wenliang Zhong and James Kwok

Fast Stochastic Alternating Direction Method of Multipliers (pdf)

We propose a new stochastic alternating direction method of multipliers (ADMM) algorithm, which incrementally approximates the full gradient in the linearized ADMM formulation. Besides having a low per-iteration complexity as existing stochastic ADMM algorithms, it improves the convergence rate on convex problems from $\mO(1/\sqrt{T

-

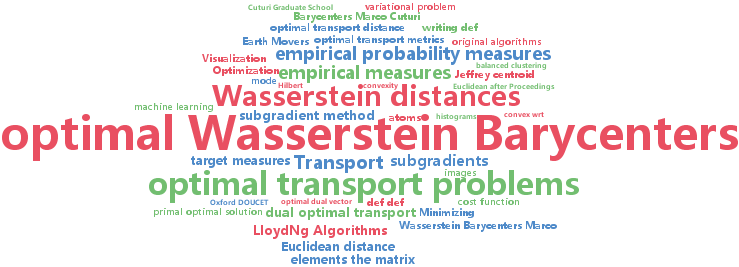

Marco Cuturi and Arnaud Doucet

Fast Computation of Wasserstein Barycenters (pdf)

We present new algorithms to compute the mean of a set of $N$ empirical probability measures under the optimal transport metric. This mean, known as the Wasserstein barycenter~\citep{agueh2011barycenters,rabin2012

-

Michalis Titsias and Miguel Lázaro-Gredilla

Doubly Stochastic Variational Bayes for non-Conjugate Inference (pdf)

We propose a simple and effective variational inference algorithm based on stochastic optimisation that can be widely applied for Bayesian non-conjugate inference in continuous parameter spaces. This algorithm is based on stochastic approximation and allows for efficient use of gradient information from the model joint density. We demonstrate these properties using illustrative examples as well as in challenging and diverse Bayesian inference problems such as variable selection in logistic regression and fully Bayesian inference over kernel hyperparameters in Gaussian process regression.

-

Taiji Suzuki

Stochastic Dual Coordinate Ascent with Alternating Direction Method of Multipliers (pdf)

We propose a new stochastic dual coordinate ascent technique that can be applied to a wide range of regularized learning problems. Our method is based on alternating direction method of multipliers (ADMM) to deal with complex regularization functions such as structured regularizations. Although the original ADMM is a batch method, the proposed method offers a stochastic update rule where each iteration requires only one or few sample observations. Moreover, our method can naturally afford mini-batch update and it gives speed up of convergence. We show that, under mild assumptions, our method converges exponentially. The numerical experiments show that our method actually performs efficiently.

-

Yariv Mizrahi and Misha Denil and Nando De Freitas

Linear and Parallel Learning of Markov Random Fields (pdf)

We introduce a new embarrassingly parallel parameter learning algorithm for Markov random fields which is efficient for a large class of practical models. Our algorithm parallelizes naturally over cliques and, for graphs of bounded degree, its complexity is linear in the number of cliques. Unlike its competitors, our algorithm is fully parallel and for log-linear models it is also data efficient, requiring only the local sufficient statistics of the data to estimate parameters.

-

Jinli Hu and Amos Storkey

Multi-period Trading Prediction Markets with Connections to Machine Learning (pdf)

We present a new model for prediction markets, in which we use risk measures to model agents and introduce a market maker to describe the trading process. This specific choice of modelling approach enables us to show that the whole market approaches a global objective, despite the fact that the market is designed such that each agent only cares about its own goal. In addition, the market dynamic provides a sensible algorithm for optimising the global objective. An intimate connection between machine learning and our markets is thus established, such that we could 1) analyse a market by applying machine learning methods to the global objective; and 2) solve machine learning problems by setting up and running certain markets.

-

Pranjal Awasthi and Maria Balcan and Konstantin Voevodski

Local algorithms for interactive clustering (pdf)

We study the design of interactive clustering algorithms for data sets satisfying natural stability assumptions. Our algorithms start with any initial clustering and only make local changes in each step; both are desirable features in many applications. We show that in this constrained setting one can still design provably efficient algorithms that produce accurate clusterings. We also show that our algorithms perform well on real-world data.

-

Jason Weston and Ron Weiss and Hector Yee

Affinity Weighted Embedding (pdf)

Supervised linear embedding models like Wsabie (Weston et al., 2011) and supervised semantic indexing (Bai et al., 2010) have proven successful at ranking, recommendation and annotation tasks. However, despite being scalable to large datasets they do not take full advantage of the extra data due to their linear nature, and we believe they typically underfit. We propose a new class of models which aim to provide improved performance while retaining many of the benefits of the existing class of embedding models. Our approach works by reweighting each component of the embedding of features and labels with a potentially nonlinear affinity function. We describe several variants of the family, and show its usefulness on several datasets.

-

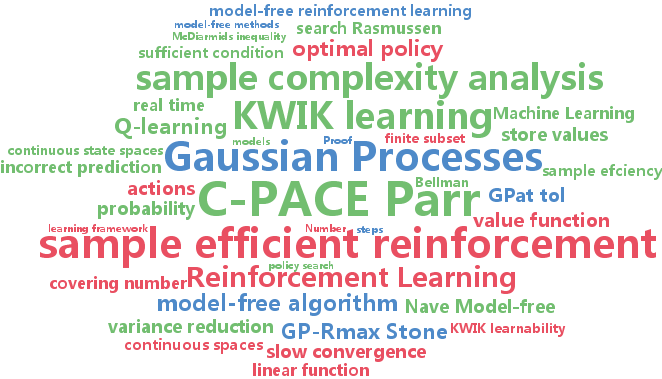

Robert Grande and Thomas Walsh and Jonathan How

Sample Efficient Reinforcement Learning with Gaussian Processes (pdf)

This paper derives sample complexity results for using Gaussian Processes (GPs) in both model-based and model-free reinforcement learning (RL). We show that GPs are KWIK learnable, proving for the first time that a model-based RL approach using GPs, GP-Rmax, is sample efficient (PAC-MDP). However, we then show that previous approaches to model-free RL using GPs take an exponential number of steps to find an optimal policy, and are therefore not sample efficient. The third and main contribution is the introduction of a model-free RL algorithm using GPs, DGPQ, which is sample efficient and, in contrast to model-based algorithms, capable of acting in real time, as demonstrated on a five-dimensional aircraft simulator.

-

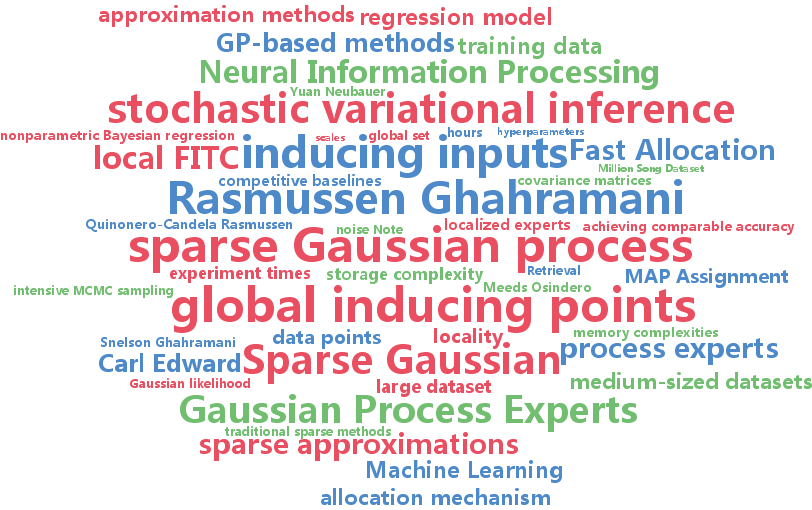

Trung Nguyen and Edwin Bonilla

Fast Allocation of Gaussian Process Experts (pdf)

We propose a scalable nonparametric Bayesian regression model based on a mixture of Gaussian process (GP) experts and the inducing points formalism underpinning sparse GP approximations. Each expert is augmented with a set of inducing points, and the allocation of data points to experts is defined probabilistically based on their proximity to the experts. This allocation mechanism enables a fast variational inference procedure for learning of the inducing inputs and hyperparameters of the experts. When using $K$ experts, our method can run $K^2$ times faster and use $K^2$ times less memory than popular sparse methods such as the FITC approximation. Furthermore, it is easy to parallelize and handles non-stationarity straightforwardly. Our experiments show that on medium-sized datasets (of around $10^4$ training points) it trains up to 5 times faster than FITC while achieving comparable accuracy. On a large dataset of $10^5$ training points, our method significantly outperforms six competitive baselines while requiring only a few hours of training.

-

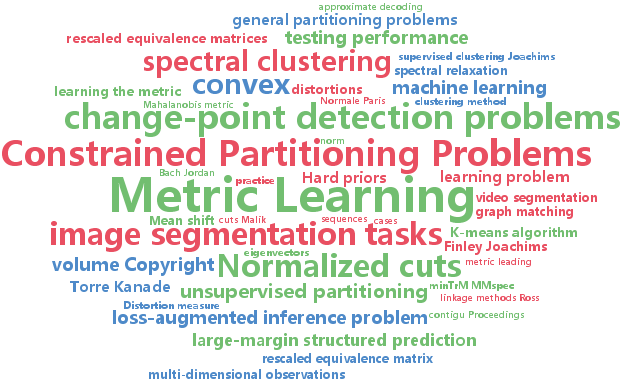

Rémi Lajugie and Francis Bach and Sylvain Arlot

Large-Margin Metric Learning for Constrained Partitioning Problems (pdf)

We consider unsupervised partitioning problems based explicitly or implicitly on the minimization of Euclidean distortions, such as clustering, image or video segmentation, and other change-point detection problems. We emphasize on cases with specific structure, which include many practical situations ranging from mean-based change-point detection to image segmentation problems. We aim at learning a Mahalanobis metric for these unsupervised problems, leading to feature weighting and/or selection. This is done in a supervised way by assuming the availability of several (partially) labeled datasets that share the same metric. We cast the metric learning problem as a large-margin structured prediction problem, with proper definition of regularizers and losses, leading to a convex optimization problem which can be solved efficiently. Our experiments show how learning the metric can significantly improve performance on bioinformatics, video or image segmentation problems.

-

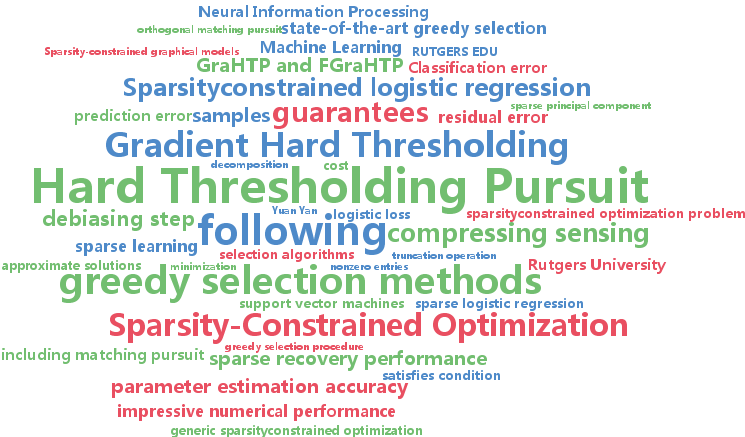

Xiaotong Yuan and Ping Li and Tong Zhang

Gradient Hard Thresholding Pursuit for Sparsity-Constrained Optimization (pdf)

Hard Thresholding Pursuit (HTP) is an iterative greedy selection procedure for finding sparse solutions of underdetermined linear systems. This method has been shown to have strong theoretical guarantees and impressive numerical performance. In this paper, we generalize HTP from compressed sensing to a generic problem setup of sparsity-constrained convex optimization. The proposed algorithm iterates between a standard gradient descent step and a hard truncation step with or without debiasing. We prove that our method enjoys the strong guarantees analogous to HTP in terms of rate of convergence and parameter estimation accuracy. Numerical evidences show that our method is superior to the state-of-the-art greedy selection methods when applied to learning tasks of sparse logistic regression and sparse support vector machines.

-

David Gleich and Michael Mahoney

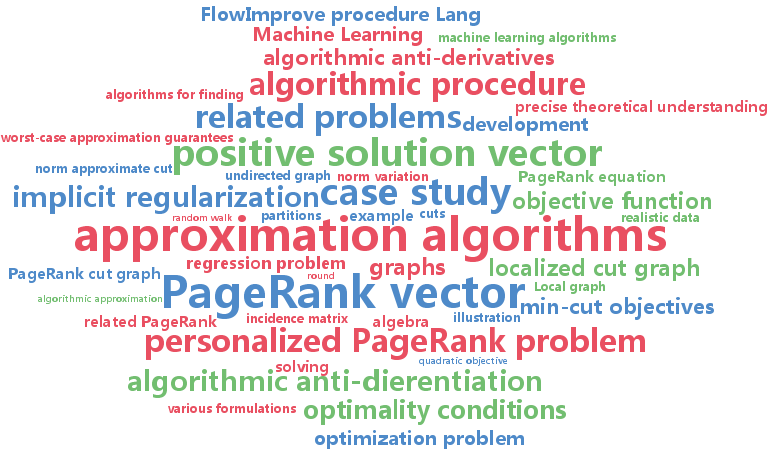

Anti-differentiating approximation algorithms:A case study with min-cuts, spectral, and flow (pdf)

We formalize and illustrate the general concept of algorithmic anti-differentiation: given an algorithmic procedure, e.g., an approximation algorithm for which worst-case approximation guarantees are available or a heuristic that has been engineered to be practically-useful but for which a precise theoretical understanding is lacking, an algorithmic anti-derivative is a precise statement of an optimization problem that is exactly solved by that procedure. We explore this concept with a case study of approximation algorithms for finding locally-biased partitions in data graphs, demonstrating connections between min-cut objectives, a personalized version of the popular PageRank vector, and the highly effective "push" procedure for computing an approximation to personalized PageRank. We show, for example, that this latter algorithm solves (exactly, but implicitly) an l1-regularized l2-regression problem, a fact that helps to explain its excellent performance in practice. We expect that, when available, these implicit optimization problems will be critical for rationalizing and predicting the performance of many approximation algorithms on realistic data.

-

Tien Vu Nguyen and Dinh Phung and Xuanlong Nguyen and Swetha Venkatesh and Hung Bui

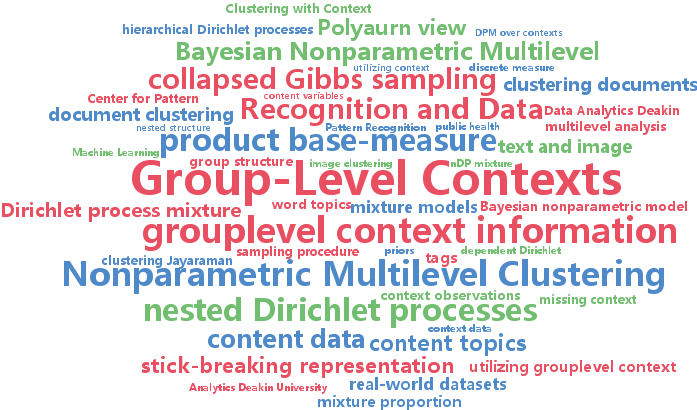

Bayesian Nonparametric Multilevel Clustering with Group-Level Contexts (pdf)

We present a Bayesian nonparametric framework for multilevel clustering which utilizes group-level context information to simultaneously discover low-dimensional structures of the group contents and partitions groups into clusters. Using the Dirichlet process as the building block, our model constructs a product base-measure with a nested structure to accommodate content and context observations at multiple levels. The proposed model possesses properties that link the nested Dirichlet processes (nDP) and the Dirichlet process mixture models (DPM) in an interesting way: integrating out all contents results in the DPM over contexts, whereas integrating out group-specific contexts results in the nDP mixture over content variables. We provide a Polya-urn view of the model and an efficient collapsed Gibbs inference procedure. Extensive experiments on real-world datasets demonstrate the advantage of utilizing context information via our model in both text and image domains.

-

Rashish Tandon and Pradeep Ravikumar

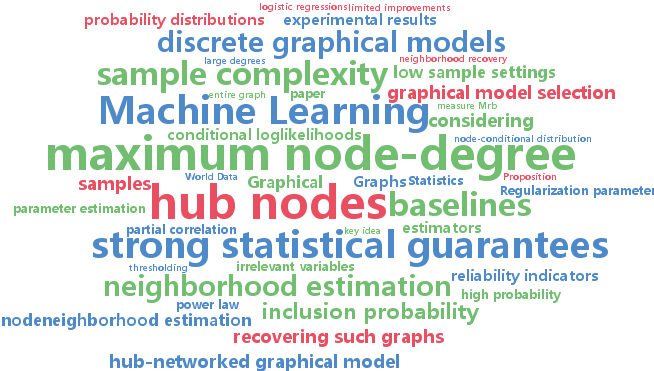

Learning Graphs with a Few Hubs (pdf)

We consider the problem of recovering the graph structure of a ``hub-networked'' Ising model given iid samples, under high-dimensional settings, where number of nodes $p$ could be potentially larger than the number of samples $n$. By a ``hub-networked'' graph, we mean a graph with a few ``hub nodes'' with very large degrees. State of the art estimators for Ising models have a sample complexity that scales polynomially with the maximum node-degree, and are thus ill-suited to recovering such graphs with a few hub nodes. Some recent proposals for specifically recovering hub graphical models do not come with theoretical guarantees, and even empirically provide limited improvements over vanilla Ising model estimators. Here, we show that under such low sample settings, instead of estimating ``difficult'' components such as hub-neighborhoods, we can use quantitative indicators of our inability to do so, and thereby identify hub-nodes. This simple procedure allows us to recover hub-networked graphs with very strong statistical guarantees even under very low sample settings.