{kind=link}

Abstract:

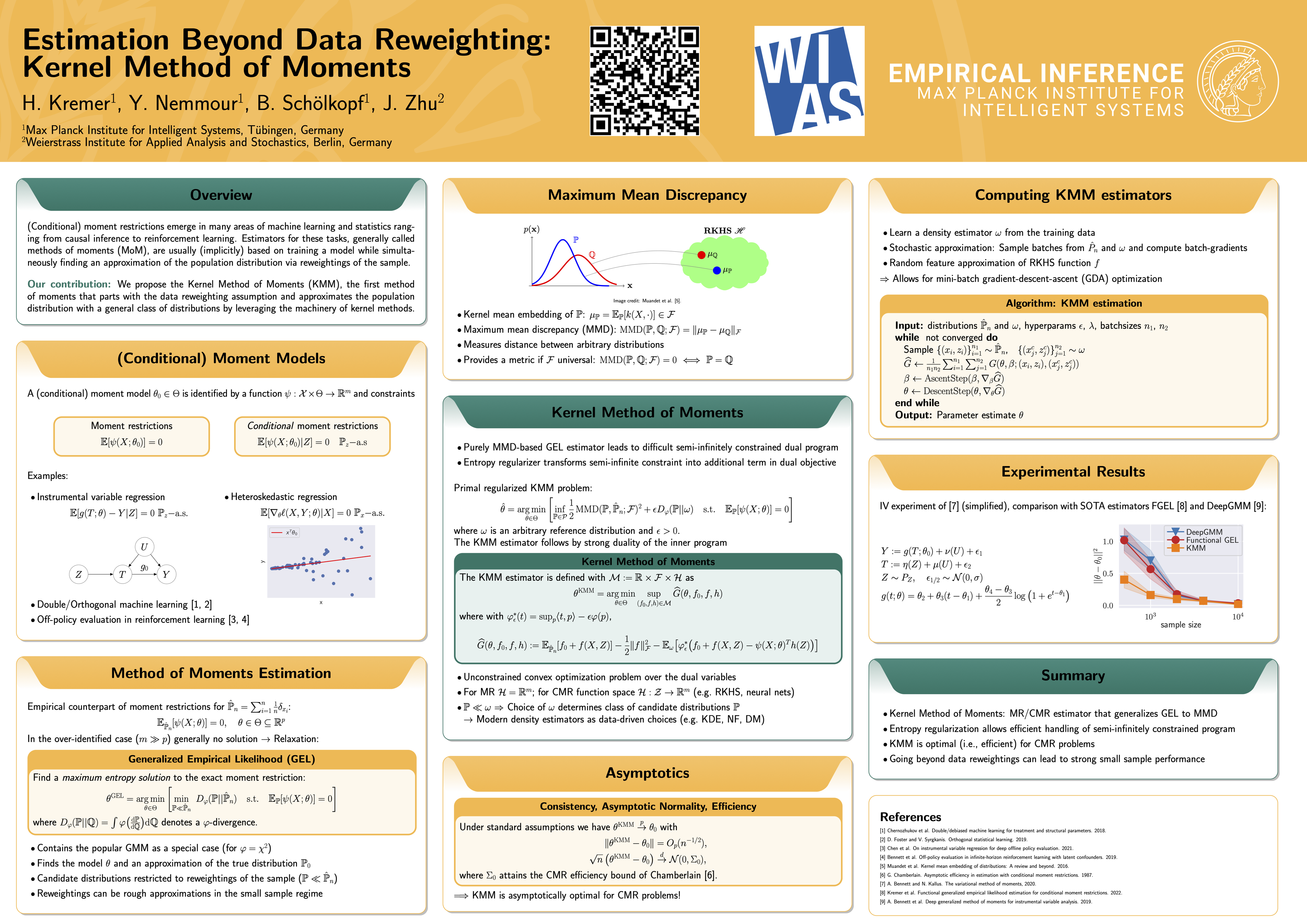

Moment restrictions and their conditional counterparts emerge in many areas of machine learning and statistics ranging from causal inference to reinforcement learning. Estimators for these tasks, generally called methods of moments, include the prominent generalized method of moments (GMM) which has recently gained attention in causal inference. GMM is a special case of the broader family of empirical likelihood estimators which are based on approximating a population distribution by means of minimizing a $\varphi$-divergence to an empirical distribution. However, the use of $\varphi$-divergences effectively limits the candidate distributions to reweightings of the data samples. We lift this long-standing limitation and provide a method of moments that goes beyond data reweighting. This is achieved by defining an empirical likelihood estimator based on maximum mean discrepancy which we term the kernel method of moments (KMM). We provide a variant of our estimator for conditional moment restrictions and show that it is asymptotically first-order optimal for such problems. Finally, we show that our method achieves competitive performance on several conditional moment restriction tasks.

Chat is not available.